Neutral TATA Motors Ltd for the Target Rs.416 by Motilal Oswal Financial Services Ltd

Rising costs to drive near-term margin pressure Growth outlook turns cautious

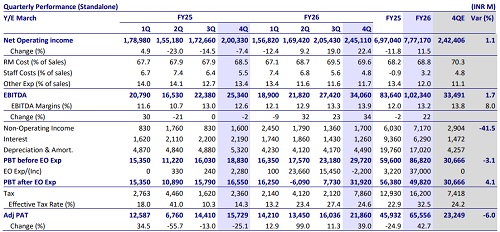

* Tata Motors’ (TMCV) 4QFY26 PAT at INR22b was below our est. of INR23b due to lower-than-expected other income, even as operational performance was in line. EBITDA margin expanded 130bp YoY to 13.9%, led by operating leverage benefits.

* Demand outlook for the domestic CV industry has turned cautious post ongoing geopolitical dynamics and the impact it may have on the Indian economy, with likely margin pressure in the near term. We have, hence, lowered our growth forecast for TMCV CV volumes to 6% CAGR over FY26- 28E from 8% CAGR earlier. We now factor in TMCV to post revenue/EBITDA/PAT CAGR of 8%/8%/10% over FY26-28E. The stock at 20.8x FY27E and at 17.9x FY28E EPS appears fairly valued. Reiterate Neutral with a TP of INR416 per share – we value the core business at 12x FY28E EV/EBITDA (in line with peers) and add INR12 per share for its stake in Tata Capital.

Earnings below estimates due to lower other income

* TMCV’s 4Q revenue grew 22% YoY to INR245b (in line), supported by 25% volume growth YoY, while ASP declined 2% YoY.

* EBITDA margins expanded 130bp YoY to 13.9% (in line), led by operating leverage benefits. EBITDA grew 34% YoY to INR34b (in line).

* The company recorded an impairment provision of INR23.1b in 4Q due to a reduction in the NAV of TMF Holdings, while labor code provisions worth INR2.11b were reversed in the quarter.

* Adjusting for this, PAT grew 39% YoY to INR22b (6% below estimates), due to lower other income and slightly higher tax rate.

* FY26 performance: Revenue/EBITDA/PAT grew 12%/22%/43%, respectively.

* OCF/FCF stood at INR113b/INR93b, respectively

Valuation and view

Demand outlook for the domestic CV industry has turned cautious post the ongoing geopolitical dynamics and the impact it may have on the Indian economy, with likely margin pressure in the near term. We have, hence, lowered our growth forecast for TMCV CV volumes to 6% CAGR over FY26-28E from 8% CAGR earlier. We now factor in TMCV to post revenue/EBITDA/PAT CAGR of 8%/8%/10% over FY26-28E. The stock at 20.8x FY27E and at 17.9x FY28E EPS appears fairly valued. Reiterate Neutral with a TP of INR416 per share – we value the core business at 12x FY28E EV/EBITDA (in line with peers) and add INR12 per share for its stake in Tata Capital.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)