Buy Waaree Energies Ltd for the Target Rs. 3,850 by Motilal Oswal Financial Services Ltd

Waaree 2.0 to power multi-year growth

* We attended Waaree Energies Limited’s (WEL) investor day, wherein management laid out an aggressive roadmap to scale revenue to INR1t by 2030, supported by a sharp acceleration across C&I, KUSUM, and rooftop solar segments. The company expects India’s annual solar demand to rise materially from ~50GW in FY27 to ~85GW by FY30, while also highlighting agri-solarisation and BESS as major long-term opportunities. Management emphasized that technology transition, backward integration, and supply chain control will be critical to maintaining competitiveness amid industry overcapacity and pricing volatility. We maintain our BUY rating on WEL with an SOTP-based TP of INR 3850.

* Management targets INR1t revenue by 2030; growth visibility improving across segments - Management outlined an ambitious aspiration to scale revenue to INR1t by 2030 (~4x) and provided granular details across various growth pillars expected to drive this expansion. The company highlighted strong visibility across utility, C&I, and distributed solar segments, alongside a clear strategic roadmap focused on integration, technology leadership, and manufacturing scale-up.

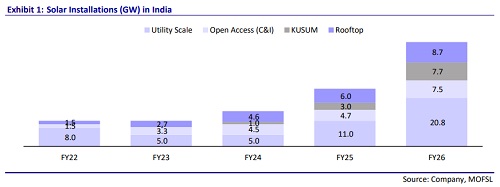

* C&I, KUSUM, and rooftop solar witnessing a sharp acceleration - A meaningful acceleration is expected in FY27, particularly in the C&I and KUSUM segments (C&I/KUSUM installations increased from ~4.7/3GW in FY25 to ~7.5/7.7GW in FY26). Management also highlighted agrisolarisation as a massive long-term opportunity, estimating a potential market size of ~191GW assuming full solarization. In rooftop solar, PM Surya Ghar momentum continues to strengthen, with installations expected to rise from ~8.7GW in FY26 to ~10GW in FY27, while the application pipeline already stands higher at ~11.5GW.

* Backward integration critical to long-term competitiveness: Management emphasized that staying relevant will require continuous technology transition and deeper backward integration. Capex intensity has increased nearly 10x over the last decade, rising from INR1.5b/GW for module-only facilities to INR16b/GW for fully integrated polysilicon-to-module operations.

* Commodity and overcapacity risks being addressed proactively: To reduce exposure to commodity price volatility and tariff-related risks, WEL has taken a stake in an Oman-based company with exposure across the polysilicon value chain. Management also believes that continued backward integration and migration toward premium technologies will help counter industry overcapacity risks. * BESS emerging as a key long-term growth driver: Battery energy storage systems (BESS) remain another key growth pillar for WEL. Management highlighted plans to build India’s first fully integrated gigafactory spanning cell manufacturing to containerized BESS solutions, with an aim to become a fully integrated 20GWh player by 2028.

Waaree 2.0: Building a full stack

* Management outlined its long-term ‘Waaree 2.0’ roadmap (requiring capex of INR320b over the next two years), targeting the creation of a fully integrated clean energy manufacturing ecosystem comprising: * 28GW module manufacturing capacity,

* 15GW cell manufacturing capacity,

* 10GW ingot-wafer capacity,

* 20GWh BESS manufacturing facility,

* 4GW inverter manufacturing capacity,

* 20,000MVA transformer manufacturing capacity,

* 1GW electrolyser manufacturing capacity,

* 2,500TPD solar glass manufacturing,

* Polysilicon manufacturing capabilities.

Scale, margins, and discipline: The path to INR1t topline

* Management guided for ~20% EBITDA margins, noting that some of the company’s newer business verticals may operate at relatively lower margins initially.

* The company currently commands ~15–18% market share in India’s solar industry.

* Employee count has increased from less than 2,000 historically to ~12,000– 13,000 currently and is expected to reach ~20,000 over the next 2–3 years.

Management reiterated its intention to maintain a debt-to-equity ratio below 1x even over the long term.

* Management outlined a medium-term revenue aspiration of ~INR1t over the next five years vs FY26 revenue of ~INR265b.

Global renewable energy deployment accelerating

* Global electrification is accelerating, driven by increasing electrification of enduse applications such as air conditioning, EV charging, and industrial processes, alongside the rising share of renewable energy in power generation.

* The global solar industry required nearly 22 years to install its first 1TW of capacity, while the next 2TW is expected to be added within just five years. Annual solar installation rates have accelerated, with the world now adding ~1GW of solar capacity every 12 hours. ? Global annual solar investments have reached ~USD500b, with ~50% directed toward rooftop and commercial & industrial (C&I) solar segments.

India's renewable runway: From 150GW to 1,200GW

* India’s installed solar capacity currently stands at ~150GW and is projected to scale to ~400GW over the next seven years and ~1,200GW over the next 25 years.

* India’s battery storage market is expected to expand from ~1GWh currently to more than 200GWh over the next seven years.

* Renewable energy’s share in India’s installed capacity is expected to rise to ~66% by 2032 and ~85% by 2047.

* Renewable energy currently contributes ~14% to India’s electricity generation mix compared with ~19% in the US, ~22% in China, and ~30% in Europe, indicating significant headroom for growth.

India Solar: Policy, cost, and scale firing in unison Management highlighted multiple structural drivers supporting India’s solar capacity expansion toward ~341GW by 2030:

* Strong government policy support, PM Surya Ghar scheme, PLI incentives, and the 500GW non-fossil fuel capacity target by 2030.

* Rapid domestic manufacturing scale-up, with module capacity expected to rise from ~80GW to ~160GW and cell capacity from ~15GW to ~120GW by 2030.

* Continued decline in solar power costs, with tariffs now at ~INR2.5/kWh following a ~90% reduction in costs since 2010. * Strong rooftop solar momentum driven by PM Surya Ghar’s target of solarizing 10m households, with distributed solar installations growing ~23% YoY.

* Storage-led integration of renewable energy, with India expected to add ~232GWh of storage capacity by 2032 to support grid stability and reduce renewable curtailment.

Rooftop, C&I, and KUSUM opportunity

* Annual installations across rooftop solar, C&I, and KUSUM segments increased from ~10GW in FY24 to ~24GW by FY26.

* Management highlighted India’s underpenetrated rooftop market, with only ~1% of rooftops solarized vs ~21.5% in Japan, ~12% in Germany, and ~24% in the Netherlands.Manufacturing scale and capital intensity * Management highlighted the sharp increase in capital intensity as manufacturers move up the solar value chain:

* ~INR1.5b capex required for 1GW module manufacturing capacity.

* ~INR6b for integrated cell + module capacity.

* ~INR12b for cell + module + ingot-wafer integration.

* ~INR16b for fully integrated polysilicon-to-module capacity.

* Management believes only a limited number of players possess the scale, balance sheet strength, and execution capabilities required for full backward integration.

* Management highlighted that only four companies outside China currently operate polysilicon manufacturing facilities, located in Germany, the US, Malaysia, and Oman (the one in which WEL has invested INR2.7b).

US Capacity: Scaling to 4.6GW amid import dependency

* The US solar market currently represents an annual demand of ~50–60GW, with ~80–85% dependent on imports.

* WEL highlighted its US module capacity to reach 4.6GW (vs. 1.6GW now) in the next six months, with further capacity expansion planned.

Solar + Storage: WEL bets on the winning combo

* Management emphasized that Solar + BESS is emerging as the preferred renewable energy architecture globally, citing China as a leading example.

* WEL is developing a 3.5GWh integrated BESS manufacturing facility in Valsad covering cell-to-pack and containerized storage systems. The company targets scaling BESS capacity to ~20GWh by FY28.

* Key sector tailwinds include VGF support, PLI incentives for ACC batteries, dedicated BESS schemes, and the broader ‘Make in India’ push.

Valuation and view

* The valuation of WEL has been derived through a sum-of-the-parts (SoTP) methodology, resulting in a TP of INR3,850/share.

* The domestic module business is valued at 13x FY28E EBITDA. The US module business is valued at 12x FY28E EBITDA, which is in line with global peers. The new business segment, valued at 10x FY28E EBITDA, is consistent with domestic peer valuations. The sum of these segment valuations (adjusting for net debt) results in a TP of INR3,850/share.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412