Neutral KNR Constructions Ltd for the Target Rs.130 by Motilal Oswal Financial Services Ltd

Weak execution yet again; revenue to improve as execution of recent orders picks up

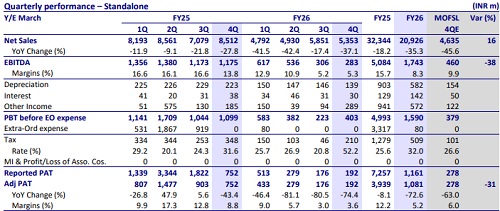

* KNR Constructions (KNRC)’s revenue declined ~37% YoY to ~INR5.3b during 4QFY26 (16% above our estimate).

* EBITDA margin decreased 850bp YoY to 5.3% (vs. our estimate of 9.9%) in 4QFY26. EBITDA fell ~76% YoY to INR283m (vs. our estimate of INR460m).

* In line with weak operating performance, APAT decreased ~74% YoY to INR192m (against our estimate of INR278m).

* The board also recommended a dividend of INR0.25 per share.

* In FY26, revenue/EBITDA/APAT fell ~35%/~66%/~73%.

* The company’s current order book stands at ~INR86.7b, including INR35.5b from the mining project.

* KNRC delivered a disappointing performance yet again in 4QFY26, missing estimates by a wide margin as execution slowed due to a thin executable order book. However, order awarding activity improved during the quarter, with KNR emerging as L1 in projects worth INR32.3b. We expect revenue to improve only in FY28 as recently won orders move into execution. We cut our earnings estimates for FY27 and FY28 by 8% and 3%, respectively, factoring in weak execution, and expect revenue and EBITDA CAGR of 22% and 45%, respectively, over FY26-FY28. We reiterate our Neutral rating on the stock with our SoTP-based TP of INR130.

Key takeaways from the management commentary

* Road sector witnessed muted project awarding activity during FY26, with both MoRTH and NHAI showing slower award conversion despite a healthy pipeline of ~INR3.5t due to extended approval timelines and land acquisition challenges.

* Of the revised INR9.52b equity requirement for HAM projects, INR7.3b has been infused to date, with the balance INR2.2b to be invested.

* Management has guided for order inflows of INR80-100b and revenue of ~INR20b in FY27, and expects EBITDA margin to remain in the range of 10%- 11% based on the current executable order book.

Valuation and view

* KNRC delivered a disappointing performance yet again in 4QFY26, missing estimates by a wide margin. We expect execution to pick up only from FY28 as recently won projects move into execution. We expect revenue and EBITDA CAGR of 22% and 45%, respectively, over FY26-FY28 on a low base of FY26.

* We reiterate our Neutral rating on the stock with an SoTP-based TP of INR130.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412