Buy Ipca Laboratories Ltd for the Target Rs.1,730 by Motilal Oswal Financial Services Ltd

Domestic/exports formulation drive earnings

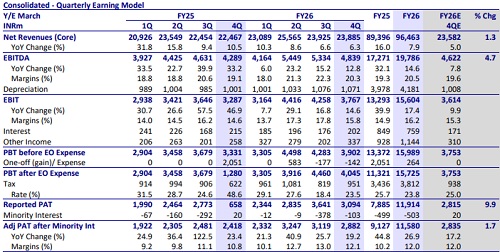

* Ipca Laboratories (IPCA) delivered in-line revenue in 4QFY28. It delivered 5% beat on EBITDA, driven by higher gross margin. PAT came in line with estimate. Revenue growth YoY was driven by domestic formulation (DF) and exports (generics and branded). This was partly offset by subdued API and institutional anti-malaria sales.

* IPCA has been consistently outperforming IPM in DF segment for four consecutive years. Its focus on core brands and limited new launches should help to sustain growth momentum going forward.

* With a gradual revival in US sales and healthy traction in other export markets for generics segment, IPCA delivered better YoY growth in generics exports for FY26.

* The branded export segment saw an uptrend in YoY growth for the third consecutive year in FY26.

* API sales have seen some moderation in the past two quarters. Having said this, it is implementing efforts to increase offtake of existing molecules and add new molecules in this segment. * We largely maintain our estimates for FY27/FY28. We value IPCA at 28x 12- month forward earnings to arrive at a TP of INR1,730.

* We expect 17% earnings CAGR over FY26-28, driven by 12% CAGR in DF revenue, 20% CAGR in exports and better operating leverage. Overall, IPCA remains in good stead for superior execution in DF and export markets, sustaining the mid-teen return ratios over FY26-28. Maintain BUY

Highlights from the management commentary

* On a consolidated basis (Ipca USA and Unichem USA combined), US business revenue stood at INR4.3b in 4QFY26 versus INR3.9b in 4QFY25, reflecting ~10% YoY growth. For FY26, US revenue was INR15.7b compared with INR13.8b in FY25, representing ~14% YoY growth.

* Management indicated that if current petroleum price trends persist, overall raw material costs could increase by ~10-12%. The company highlighted significant price increases in key inputs such as paracetamol and metformin, with the overall market witnessing raw material cost inflation of ~10-12%.

* Management indicated the scope of passing the RM price hike to customers, thereby keeping margins intact for IPCA. For generics business, the freight cost is borne by customers and thus has limited impact on IPCA’s profitability.

Valuation and view

* We largely maintain our estimates for FY27/FY28. We value IPCA at 28x 12- month forward earnings basis to arrive at a TP of INR1,730.

* We expect 17% earnings CAGR over FY26-28, driven by 12% CAGR in DF revenue, 20% CAGR in exports and better operating leverage. Overall, IPCA remains in good stead for superior execution in DF as well as exports markets, sustaining the mid-teens return ratios over FY26-28. Maintain BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412