Buy Glenmark Pharma Ltd for the Target Rs.2,610 by Motilal Oswal Financial Services Ltd

A mixed quarter; US/DF underperforms for the quarter

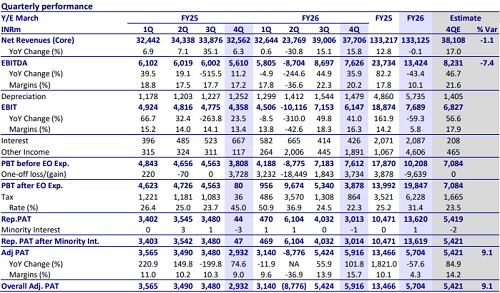

* Glenmark Pharma (GNP) delivered lower-than-expected financial performance for the quarter. While revenue was in line with our estimate, EBITDA was a 7% miss. Higher other income led to a 9% beat on PAT for the quarter. Domestic formulation (DF) and US traction were lower than expectations, while ROW/EU revenue was better than expectations for the quarter.

* US revenue growth (ex-out-licensing income) is expected to pick up over the medium term. Certain approved products and upcoming niche approvals are expected to considerably scale up the US business in FY27. Logistics disruption due to the Middle East issue impacted the US segment’s performance in 4QFY26.

* GNP outperformed IPM in the DF segment as per IQVIA, led by superior execution in cardiac, derma, and respiratory therapies. GNP’s growth was impacted by higher traction in superior molecules within diabetes therapy.

* GNP continues to expand its differentiated product offerings across the EU/emerging markets. The company is gearing up to launch products like Winlevi/Rylatris (in various EU markets) in FY27, as well as working on filing products like Qinhayo, Trastuzumab Rezertecan, and Aumolertinib for several emerging markets.

* We slightly tweak our earnings estimate upwards for FY27/FY28, factoring in:

a) An improved growth outlook for the US segment

b) Outperformance in the DF segment

c) Increased R&D spend. We value GNP at 25x 12M forward earnings to arrive at a TP of INR2,610.

* Following a strategic reset in FY26, GNP is working to scale up business across focus markets through an expanding product pipeline (respiratory/injectables for US market), and differentiated branded products in DF and EMs. Accordingly, we expect a considerable scale-up in GNP’s financial performance over FY26-28. Reiterate BUY.

Improved segmental mix drives profitability on a YoY basis

* GNP's sales grew 15.8% YoY to INR37.7b (our est. INR38.1b).

* Gross margin expanded 235bp YoY to 68.9%.

* EBITDA margin expanded 300bp YoY to 20.2% (our est. 21.6%).

* EBITDA increased 35.9% YoY to INR7.6b (our est. INR8.2b).

* GNP had exceptional items amounting to INR3.7b, largely related to litigation settlements.

* Adjusting for the same, PAT stood at INR5.9b, up 101.8% YoY (our est.: INR5.4b). PAT increased at a higher rate due to higher other income.

* For FY26, revenue was stable, while EBITDA/PAT declined 43%/58% YoY, mainly due to the impact of weak operational performance in 2QFY26

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd