Buy Container Corporation Ltd for the Target Rs. 600 by Motilal Oswal Financial Services Ltd

Structural tailwinds after WDFC connectivity

* The DFCCIL has commissioned the Western Dedicated Freight Corridor (WDFC), including the key connectivity to JNPT via Vaitarna, completing the ~2,843km DFC network. This is expected to drive a structural shift in rail logistics, with JNPT’s rail coefficient likely increasing materially from the current levels of 16%. The improvement will be supported by double-stack container movement and faster evacuation, leading to a meaningful modal shift from road to rail.

* Concor (CCRI) stands to be a key beneficiary of this transition, given its dominant 55-60% market share in rail container logistics. The all-India major port container volume stood at 213mt in FY26, growing 10% YoY.

* CCRI delivered a steady performance in terms of volume growth in FY26. The company reported ~10% YoY volume growth in FY26, with EXIM volumes growing ~8% and domestic volumes ~15%, while EXIM continues to contribute ~75% of total volumes. However, realizations in both EXIM and domestic segments remained under pressure in 9MFY26. Growth was impacted by ongoing geopolitical tensions and heightened competitive intensity, while the company continued to avoid low-margin business, leading to lower realizations.

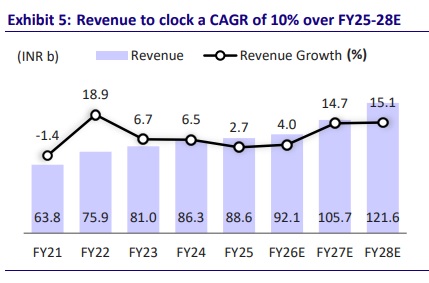

* However, we remain optimistic about CCRI’s growth outlook, supported by the commissioning of WDFC connection to JNPT, which is expected to drive volume growth and enable a more sustainable growth trajectory. We expect CCRI to clock a CAGR of 10%/11% in revenue/EBITDA over FY25- FY28. We reiterate our BUY rating on the stock with a TP of INR600 (based on 14x EV/EBITDA on FY28E).

WDFC tailwinds underpin strong FY29 growth path

* Management sees a significant opportunity in cement container transport, as only ~10% of cement is currently transported by rail, with the balance moving by road. To tap this opportunity, the company has signed MoUs with Ultratech and Adani Cement to transport 1 lakh tons of cement per month with each of them.

* CCRI had signed an MoU for developing and managing Common Rail handling operations at Vadhvan port, which is expected to be commissioned by 2030. Total project investment amounts to ~INR5b.

* The company targets strong revenue growth of ~INR150b in FY29, driven by robust traction in both EXIM and domestic segments. EXIM revenue is expected to grow at ~15% CAGR through FY29, supported by WDFC commissioning, ramp-up in double-stack volumes from Ahmedabad and Jodhpur, and throughput from new terminals at Mandalgarh, Jajpur, and Kadakola. Domestic revenue is guided to post ~20% CAGR through FY29, aided by incremental volumes from cement tank container contracts with UltraTech, JK Cement, and Adani Cement.

Valuation and view

* CCRI strengthened its logistics ecosystem by expanding double-stack rail operations, shipping operations in the Middle East, utilizing the DFC to drive efficiency, and advancing its integrated logistics network. The company remains focused on scaling up its rail freight services and infrastructure, supported by a higher capex allocation toward new terminal commissioning, fleet augmentation, and enhanced multimodal connectivity.

* We remain optimistic about the expected improvement in rail coefficient, coupled with operational efficiencies from double-stack movement and network expansion on the volume growth, supported by the commissioning of WDFC. We expect CCRI to clock a CAGR of 10%/11% in revenue/ EBITDA over FY25- FY28. We reiterate our BUY rating with a revised TP of INR600 (based on 14x EV/EBITDA on FY28E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412