Buy ICICI Lombard Ltd for the Target Rs. 2,230 by Motilal Oswal Financial Services Ltd

All engines on fire for profitable growth!

* ICICI Lombard (ICICIGI) is witnessing a sharp recovery in growth momentum, with 2HFY26 GWP growth of ~16% (vs industry ~11%), driven by a revival in motor, strong traction in health post GST changes, and steady commercial lines. The company is well-positioned to sustain midteen growth with strengthening demand across segments.

* The company is rapidly scaling its retail health franchise, led by the success of its flagship ‘Elevate’ product (retail health market share of 4.1% in FY26 from 3.2% in FY25). Fresh business growth in retail health and continued momentum in group health are likely to drive ~20% CAGR in the health segment over FY26-28, along with an improvement in profitability.

* Recovery in vehicle sales and improving pricing discipline are driving a revival in motor OD for ICICIGI, a trend expected to continue (10% FY26-28 CAGR) as pricing stabilizes. Motor TP remains a stable contributor, with rate hikes continuing to be the key driver of growth and profitability in this segment.

* ICICIGI maintains leadership across commercial segments, supported by a strong underwriting track record in claim-heavy businesses. With rate hardening, rising infrastructure capex, and increasing risk awareness, commercial lines are poised for steady growth, with improving profitability providing a stable and scalable earnings pillar.

* We expect ICICIGI’s GWP/PAT to expand at an FY26-28 CAGR of 13%/19% as CoR reduces to 101.8% by FY28. The stock has corrected in the past few months and is currently trading at 22x FY28E P/E, compared to the fiveyear average of one-year forward P/E of 35x. Reiterate a BUY rating on the stock with a TP of INR2,230 (based on 28x FY28E EPS).

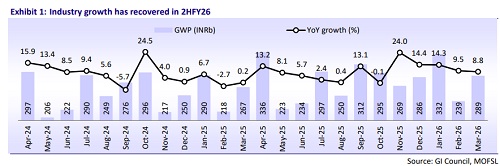

Growth recovery for private multi-line insurers

* The general insurance industry has witnessed a clear recovery in growth momentum over the past few months, with GWP growing 11% YoY in 2HFY26, following a muted FY25 (6% YoY GWP growth) and 1HFY26 (7% YoY GWP growth).

* Over the last four months, private multi-line insurers have started outperforming the industry after a slowdown in FY25 and 1HFY26. Since Nov’25, their GWP has reflected an alpha of 1-10% over industry growth.

* The growth is driven by: 1) 1/n impact on base, 2) strong traction in health insurance following GST exemption, 3) recovery in vehicle sales boosting motor insurance growth (highlighted in our sector update), and 4) sustained capex activity.

* Overall, the private GI industry appears to be transitioning back to a midteen growth trajectory, with all underlying parameters seeing favorable developments. Potential regulations on commission capping/deferment of commissions could pose a near-term threat to distribution expansion across the insurance industry.

ICICIGI’s growth trajectory improved in 2HFY26

* ICICIGI’s growth trajectory has improved from 8%/-1% in FY25/1HFY26 to 16% in 2HFY26, leading to market share improvement of 20-60bp YoY over the past few months. As of FY26, the insurer maintains the top position within the private insurance segment, with a market share of 8.9% (excluding crop insurance).

* Strong underlying demand has been observed across both motor and health following GST changes, and management intends to grow 100–200bp faster than the industry in FY27, while maintaining an 18-20% RoE. As of 2HFY26, ICICIGI has reported ~500bp alpha over industry growth. We expect its GWP to expand at an FY26-28 CAGR of 13%, with RoE in the 18-19% range.

* ICICIGI’s motor segment market share has slightly reduced over the years, from 12% in FY20 to 10.7% in FY26. However, the insurer maintains the top position. Rising competitive intensity has impacted the motor OD segment’s market share, while the motor TP segment’s market share has remained stable.

* Retail health, which is dominated by SAHIs, has been the fastest-growing segment for the insurer, growing 51% YoY during FY26YTD, backed by its flagship product ‘Elevate’. Following its launch in mid-2024, the new product has expanded retail health market share from 2.9% in FY24 to 4.1% as of FY26. ICICIGI is the largest private multi-line group health insurer, holding a stable market share of ~8.7%.

* In addition, ICICIGI is the largest private insurer in the fire segment with a stable market share in the 12.5%-13% range over the years.

Commercial lines – Maintaining the top position across segments

* Commercial lines contribute ~20% of ICICIGI’s GWP, with the insurer consistently maintaining the top position in fire, engineering, marine, and liability segments among private players.

* The SME segment represents a large, underpenetrated opportunity within commercial lines. ICICIGI is developing simplified, digitally distributable property and liability products for small businesses, which can add significant volume without the heavy loss risk of large industrial accounts.

* In the fire segment, which is the largest within commercial lines (46% of commercial GWP in FY26), ICICIGI has maintained a market share of over 12.5%, with GWP expanding at an FY20-25 CAGR of 12% and FY26 YoY growth of 8%.

* However, aggressive pricing prior to last year’s rate hardening resulted in a market share decline from 13.1% in FY24 to 12.4% in FY26, as management deliberately refrained from pursuing unprofitable business.

* With reinsurance rates hardening, ICICIGI’s growth trajectory in the fire segment has improved in FY26, as the business turned profitable. However, potential discounting in renewal pricing will likely impact the growth trajectory going ahead.

* ICICIGI’s strong balance sheet and robust underwriting capabilities position it as a strong player in the claim-heavy commercial insurance segment. Continued government-led infrastructure capex, the emergence of new-age risks such as cyber threats, and rising corporate risk awareness together underpin a compelling long-term structural opportunity for the company.

* We expect fire GWP to remain stable, with an FY26-28 CAGR of 8%. Retention is expected to be maintained at 20%, leading

Growth along with continued improvement in CoR

* We expect ICICIGI’s overall GWP to expand at an FY26-28 CAGR of 13% on the back of: 1) recovery in the motor insurance segment, 2) strong traction in retail health, and 3) stable momentum in commercial lines.

* ICICIGI’s combined ratio has increased YoY in FY26 to 103.4% (102.4% excluding the impact of 1/n), compared to 102.8% in FY25, after witnessing continued YoY improvement since FY22. This was due to: 1) high competitive intensity in motor insurance, 2) investments toward the expansion of retail health distribution capabilities, and 3) rise in fresh business growth post GST exemption.

* Going forward, the loss ratio is expected to gradually improve to 70.2% by FY28, backed by strong underwriting capabilities and growth in fresh business. Additionally, slight improvement in expense ratio is expected to take the combined ratio to 101.8% by FY28.

Valuation and view

* ICICIGI has witnessed growth recovery in 2HFY26, supported by multiple tailwinds, such as GST exemption on health insurance, strong vehicle sales after GST cuts, and continued momentum in infrastructure spending.

* While the competitive intensity remains elevated in the motor segment, the industry’s need for profitable growth to comply with EoM regulations has opened up more profitable cohorts for ICICIGI.

* GST 2.0 has proven to be a boon for the company’s fast-growing retail health segment, with profitability improving on the back of rising sum assured as well as stronger fresh business growth.

* The fire segment, which has been growing at a steady pace, is expected to maintain the growth trajectory with ICICIGI well-positioned to capture the profitable cohorts. However, discounting in the segment will keep the growth in single digits.

* We expect ICICIGI’s GWP/PAT to expand at an FY26-28 CAGR of 13%/19% as CoR reduces to 101.8% by FY28. The stock has corrected in the past few months and is currently trading at 22x FY28E P/E, compared to the five-year average of oneyear forward P/E of 35x. Reiterate a BUY rating on the stock with a TP of INR2,230 (based on 28x FY28E EPS).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

Tag News

Life Insurance Sector Update : New business in Jul-26 - Slowdown in growth momentum by Emkay...