Buy Sobha Ltd for the Target Rs.1,720 by Motilal Oswal Financial Services Ltd

Sustained launch momentum underpins pre-sales

Healthy launch pipeline and pre-sales visibility

Sobha (SOBHA) launched three new projects in 4Q – Sobha Rivana in Greater Noida (INR39b GDV), Sobha Altair in East Bengaluru (INR7b GDV), and Sobha Woods Whispering Hill in Trivandrum (INR3b GDV). The company has maintained a healthy business development and launch pipeline, with a total project pipeline of ~31.2msf, including ~20.7msf of upcoming residential developments, of which ~15msf is concentrated in Bengaluru. It has outlined ~10msf of launches for FY27 across Bengaluru, Gurugram, Hyderabad, and Pune, with additional phases planned in Kerala (including Calicut) and Bengaluru, while Chennai and Pune launches are expected subsequently. Phase 1 of the Gurugram project (Crescent), launched in Apr’26, has already achieved ~50% sales, indicating strong demand traction. Further, Phase 1 developments in Hoskote and Gurugram together account for ~6.2msf, supporting near-term visibility. SOBHA continues to invest in land acquisition, with ~INR11.5–11.6b deployed in FY26 and a similar outlay planned for FY27, targeting ~10msf addition annually.

Pre-sales momentum to remain strong

SOBHA reported pre-sales of INR20.4b in 4QFY26, up 11% YoY, with the company’s share at INR16.3b (+19% YoY), supported by sustenance sales and new launches. Rivana in Greater Noida witnessed strong initial traction with ~25% of inventory sold within the first few weeks of launch. For FY26, the company achieved healthy pre-sales of INR81.4b, up 30% YoY, driven by volumes of ~5.5msf (+18.5% YoY) and a 9% YoY increase in realizations to INR14,675/sft. Sales remained well diversified, with Bengaluru contributing ~55%, NCR ~30%, Kerala ~10%, and other cities ~5%. The company has guided for ~30% YoY growth in pre-sales for FY27, supported by a robust launch pipeline, with ~50–55% of sales expected from new launches and the balance from sustenance sales. With new launches planned and improved affordability, we bake in a 20% CAGR in pre-sales over FY26-28 at INR116b.

Healthy collections growth and cash generation

Completions during the quarter stood at 1,088 homes (~1.76msf), whereas in FY26, it completed 3,188 homes (~5.4msf). In 4QFY26, collections increased 14% YoY to INR18b, with total cash inflow (incl. contractual business) increasing by 11% YoY to INR20b. In FY26, collections grew 27% YoY to INR71b, while net operating cash flow (before interest and taxes) grew by 35% YoY to INR19b. In FY26, land-related investment stood at ~INR11.7b, up 23% YoY, while the company generated a cash surplus of INR1.7b. SOBHA’s net cash on balance sheet improved to INR8b in FY26. With construction progressing swiftly, we bake in an 18% CAGR in collections over FY26-28 at INR98b.

P&L performance

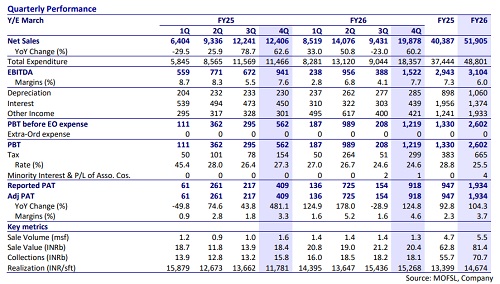

* In 4QFY26, consolidated revenue increased 60% YoY to INR19.9b, while real estate revenue also rose 69% YoY to INR17.9b. EBITDA increased 62% YoY to INR1.5b, while margin came in at 8%. Margin for the Real Estate business stood at 9%. Adj. PAT stood at INR918m, up 2x YoY. PAT margin stood at 4.6%.

* In FY26, revenue rose 29% YoY to INR51.9b, while real estate revenue stood at INR44.2b, up 31% YoY. EBITDA stood at INR3.1b, up 5% YoY, with a 6% margin. Real estate margin for FY26 stood at 9%. PAT stood at INR1.9b, up 2x YoY. PAT margin stood at 3.7%.

Valuation and view

* Ongoing and upcoming projects are valued at a DCF basis of INR139b.

* We reiterate our BUY rating on the stock with a TP of INR1,720, indicating a 19% upside potential.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412