Sell MRF Ltd for the Target Rs. 113,936 by Motilal Oswal Financial Services Ltd

Margin pressure drives earnings miss

Sharp surge in input costs to hurt performance in the near term

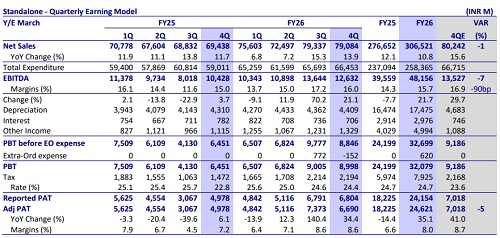

* MRF’s 4QFY26 adj PAT at INR6.7b was below our estimate of INR7b. While revenue was largely in line with our estimate, PAT miss was led by lowerthan-expected EBITDA margin at 16% (estimate of 17%).

* Management remains cautious about the demand outlook given the risk of a sub-normal monsoon. Further, rising raw material costs and supply chain disruptions due to the ongoing Middle East conflict remain key near-term headwinds. As a result, we expect MRF to post just 1% earnings CAGR over FY26-28E. While its RoCE has improved to 11.8% from a recent dip to 10% in FY25, it is likely to decline back to 10% by FY27E. Given its sub-par returns, valuations at 24.4x/21.7x FY27E/FY28E appear expensive. Maintain Sell with a TP of INR113,936, valued at 19x FY28E EPS.

PAT miss due to weaker-than-expected margins

* The company’s standalone revenue grew ~14% YoY (flat QoQ) to INR79b, largely in line with our estimate of INR80b. Demand buoyancy arising from reduction in GST rates continued into 4Q, which was reflected in both replacement and OE sales. OEMs also witnessed high demand in the quarter, which led to increased demand for tyres.

* The company has strengthened its positioning across both ICE and EV categories, emerging as a preferred tyre supplier for EVs while increasing fitment of its tyres on OEM vehicles exported to global markets. Capacity expansion across plants is underway to support future growth across domestic and export segments. ? MRF’s gross margin at 38.3% (+230bp YoY and +40bp QoQ) was above our estimate of 37.6%.

* However, EBITDA missed our estimates, coming in at INR12.6b, up 21.1% YoY. EBITDA margins were up 100bp YoY to 16% (though below our estimate of ~17%).

* The company recorded an exceptional charge of INR152m on account of the re-assement of the provisions for change in labor code.

* Adjusting for this charge, PAT was up 34.4% YoY at INR6.7b (vs. our estimate of INR7b).

* The board declared a final dividend of INR235 per share, flat YoY.

Valuation and view

Management remains cautious about the demand outlook given the risk of a subnormal monsoon. Further, rising raw material costs and supply chain disruptions due to the ongoing Middle East conflict remain key near-term headwinds. As a result, we expect MRF to post just 1% earnings CAGR over FY26-28E. While its RoCE has improved to 11.8% from a recent dip to 10% in FY25, it is likely to decline back to 10% by FY27E. Given its sub-par returns, valuations at 24.4x/ 21.7x FY27E/FY28E appear expensive. Maintain Sell with a TP of INR113,936, valued at 19x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412