Buy Five Star Business Finance Ltd for the Target Rs.600 by Motilal Oswal Financial Services Ltd

Subdued quarter but improving collections to support revival

Early delinquencies improved with moderation in 1+ dpd and 30+dpd

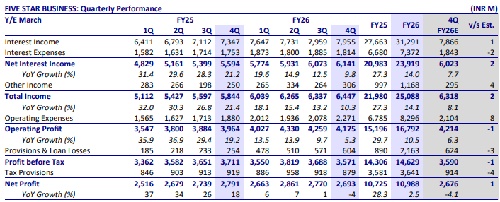

* Five-Star Business Finance’s (FIVESTAR) 4QFY26 PAT declined by 4% YoY and 3% QoQ to INR2.7b (in line). FY26 PAT grew ~2% YoY to INR11b. NII grew ~10% YoY to INR6.1b (in line). Other income rose 22% YoY to INR306m (in line).

* Opex grew 21% YoY to INR2.3b (in line). PPoP rose ~5% YoY to INR4.2b (in line). FY26 PPOP grew 11% YoY to INR16.8b. Credit costs stood at INR604m (in line). Annualized credit cost stood at ~1.55% (PQ: ~1.5% and PY: ~0.75%).

* Disbursements declined ~17% YoY and grew ~24% QoQ to ~INR12.1b. AUM grew 11% YoY/2% QoQ to ~INR132b. Management indicated that with asset quality stabilizing, the company has pivoted back toward growth and expects a strong pickup in disbursements in the coming quarters. It has guided for ~20% AUM growth, with potential upside if asset quality trends and collection efficiency continue to improve. We model AUM CAGR of ~21% over FY26-28.

* Management indicated that forward flows are moderating, which is expected to result in lower arrears and NPAs, with NPAs likely to start declining from the next quarter. The uptick in current bucket customers after several quarters of decline reflects normalization in collection cycles and borrower behavior.

* The company also shared that there has been no impact from the current geopolitical tensions so far; however, it continues to closely monitor the evolving situation.

* Five Star is making efforts to promote responsible credit behavior, aimed at creating a more resilient foundation for the medium to longer term. 1+dpd improved ~90bp QoQ, which suggests that the early-bucket delinquencies are stabilizing and if this trend continues, it will give management the confidence to accelerate disbursement growth within the next one-two quarters.

* We estimate the company to post a CAGR of ~21%/~12% in AUM/PAT over FY26-28E with FY28E RoA/RoE of 6.6%/15%. Maintain BUY with a revised TP of INR600 (based on 1.8x Mar’28E BV).

NIM expands ~50bp QoQ; incremental CoB rises ~35bp sequentially

* Reported yields declined to ~45bp QoQ to 22.6%, while CoB fell ~20bp QoQ to 8.95%. Reported spreads declined ~25bp QoQ to 13.6%. Reported NIM (as a % of AUM) rose by 50bp QoQ to ~20.1%.

* Incremental CoF rose by ~35bp QoQ to ~8.5%. The company indicated that it does not expect any meaningful benefit in its cost of funds in the coming year, given the prevailing geopolitical uncertainties.

* 4QFY26 RoAUM/RoE stood at 8.4%/15.1%. Capital adequacy stood at ~51.9% as of Mar’26.

Asset quality deteriorates but clear improvement in early delinquencies

* GS3 rose ~20bp QoQ to 3.4%, while NS3 increased 5bp QoQ to 2%. PCR rose ~155bp QoQ to ~41.4%. Stage 1 and Stage 2 PCR declined ~7bp and ~50bp QoQ, respectively.

* 30+ dpd declined ~12bp QoQ to 12.7% and 1+dpd improved ~90bp QoQ to 17.3%

* Overall collection efficiency and unique customer collection efficiency stood at 99.3% and 98.1%, respectively, in 4Q. Cash proportion in collections declined to ~16% (PQ: ~17% and PY: ~20%).

* Slippage ratio declined from 1.09% in 3QFY26 to 0.7% in 4QFY26

Highlights from the management commentary

* Management highlighted that ~85% of the portfolio remains concentrated in South India. Growth in these regions was subdued earlier due to overleverage issues, but recovery trends are now visible. FY27 growth is expected to be largely driven by southern markets (AP, Telangana, Tamil Nadu, Karnataka).

* Affordable housing loans have been launched selectively; however, the nearterm focus remains on scaling and stabilizing the core micro-LAP segment. The sweet spot for affordable housing ticket sizes is INR700k-INR1m, which the company plans to scale up gradually.

Valuation and view

* FIVESTAR reported a subdued performance during the quarter, marked by muted disbursements and AUM growth. Asset quality weakened, with an increase in both GNPA and NNPA ratios, while credit costs inched up. However, early delinquencies showed signs of improvement, with 1+dpd and 30+dpd improving during the quarter, which gives us confidence that the company will strengthen its focus on business growth in the coming quarters.

* The stock currently trades at 1.7x FY27E P/BV. We estimate FIVESTAR to post a CAGR of ~21%/~12% in AUM/PAT over FY26-28E with RoA/ RoE of 6.6/15% in FY28E. Maintain BUY with a revised TP of INR600 (based on 1.8x Mar’28E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412