Buy NMDC Ltd for the Target Rs.106 by Motilal Oswal Financial Services Ltd

Broadly in-line earnings; outlook bright with volume uptick and elevated prices

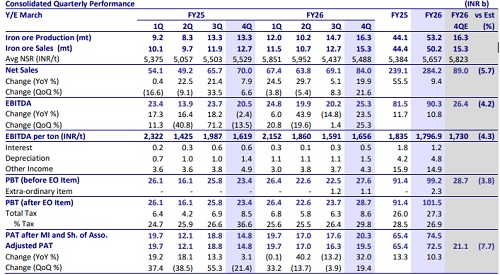

* NMDC’s reported consol. revenue stood at INR113b, driven by third-party value-added sales of INR30b in 4QFY26. The company undertook a temporary HR coil trading arrangement to support the working capital requirements of NMDC Steel. Management clarified that this was a one-off transaction and no such trading activity will be undertaken going forward.

* Revenue (ex-third party sales) stood at INR84b (vs. our est. of INR89b), growing 20% YoY and 22% QoQ, driven by better volumes during the quarter.

* Iron ore production stood at 16.3mt (+22% YoY and +11% QoQ), while sales were at 15.3mt (+21% YoY and QoQ) during the quarter.

* Blended ASP for the quarter stood at INR5,488/t (flat YoY and QoQ), while iron ore ASP stood at INR4,873/t (-3% YoY and +3% QoQ) in 4QFY26.

* EBITDA stood at INR25.3b (+24% YoY and +25% QoQ), largely in line with our estimate. EBITDA/t improved to INR1,656/t (+2% YoY and +4% QoQ) against our est. of INR1,730/t during the quarter.

* APAT for the quarter stood at INR19.5b (+32% YoY and +19% QoQ) against our estimate of INR21b during the quarter.

* In FY26, revenue stood at INR284b (+9% YoY), whereas EBITDA grew 11% YoY to INR90.3b and APAT by 10% YoY to INR72.2b. Annual production volume stood at 53.2mt (+21% YoY), and sales volume rose 13% YoY to 50mt in FY26, with blended ASP of INR5,657/t (+5% YoY)

Valuation and view

* NMDC reported strong earnings during the quarter, supported by healthy volumes. Management has guided for production volume to increase to ~60mt in FY27, fueled by an increasing EC limit and a new mine under JV. We largely maintain our estimates for FY27/28 and expect volumes and prices to remain elevated, in line with strong demand from steel makers.

* NMDC has planned a strong capex pipeline over various evacuation and capacity enhancement projects, aimed at improving the product mix and increasing production capacity to ~100mt by FY30.

* Additionally, the company is expected to venture into business diversification through coking/non-coking coal mines, critical minerals, and rare earth elements, which will serve as the catalyst for incremental revenue and EBITDA in the long term.

* At CMP, the stock trades at 6.1x EV/EBITDA and 1.7x on P/BV on FY28 estimate. We reiterate our BUY rating on NMDC with a TP of INR106 (based on 7x EV/EBITDA on FY28 estimate).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)