Buy VIP Industries Ltd for the Target Rs 430 by Motilal Oswal Financial Services Ltd

Change of control triggers renewed action

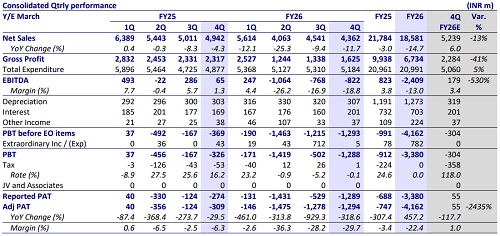

VIP Industries’ (VIP) 4QFY26 print was below our estimate, with consolidated revenue declining 11.7% YoY to INR4.4b and losses reported at EBITDA/PAT level. The revenue decline was driven by:

1) A sharp reduction in SLOB inventory

2) Weak channel partner engagement

3) Lower online sales. The company reduced SLOB inventory by INR2.3b in FY26 to introduce new trendy SKUs while tightening inventory management and increasing focus on secondary sales. EBITDA for the quarter was impacted by channel inventory liquidation support extended to channel partners, amounting to INR300m, along with one-time expenses of INR230m. We believe the company’s strategic focus on cleaning up old inventory and building a brand-focused organization is a step in the right direction and should support a stronger balance sheet. According to our channel checks, VIP has taken a 6-7% price hike effective May’26. We expect the company to deliver a 16% revenue CAGR over FY26-28.

Strategic reset to gain momentum

As highlighted in our IC and subsequently confirmed by the company, VIP has largely completed its restructuring initiatives across system inventory and management capabilities during the clean-up phase. Key focus areas included channel re-energization, SKU rationalization, and a complete brand revamp. Inventory levels were reduced sharply from 4.5m to 2.8m units, with channel inventory down to less than 60 days from ~90 days earlier. The company absorbed ~INR1.3b impact from old stock liquidation, impacting 4QFY26 margins. More than 65 new products were launched during the quarter, with premiumization initiatives underway across brands such as VIP, Skybags, Aristocrat, and Alfa, alongside a price increase of 6-7% from May. Utilization levels at the Bangladesh and Nashik facilities improved significantly to ~95%. More importantly, management indicated that secondary sales registered double-digit growth, although April remained relatively weak.

Gross margins reach 37.2% due to inventory liquidation

Gross margins stood at 37.2% (-956bp YoY & +778bp QoQ), impacted by elevated discounting on inventory liquidation. EBITDA loss was INR822m, with EBITDA margin at -18.8%, led by employee costs (+0.6%) and other expenses (+11.2%). During the quarter, the company extended ~INR300m of support toward channel inventory liquidation and incurred one-time costs of INR230m, both of which impacted EBITDA. In addition, the company reported a one-time exceptional gain of INR5m, mainly on account of an insurance claim. With the new management prioritizing inventory clean-up and re-establishing pricing discipline, we anticipate EBITDA recovery to begin from FY27 onward

Valuation and view: Reiterate BUY; expect a turnaround in 2HFY27

We expect VIP to gain market share and deliver industry-leading growth, leveraging the following strategic drivers:

1) Removal of SLOB inventory and replenishment with new trending SKUs under tighter inventory control

2) Product upgrades through distinctive features

3) Store rationalization. We remain optimistic on VIP’s growth story, and expect the company to report a revenue CAGR of 16% over FY26-28. Accordingly, we reiterate BUY with a revised TP of INR430 (implying 41x FY28E EPS). Risks: local competition and a significant rise in input costs

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412