Neutral United Spirits Ltd for the Target Rs.1,500 by Motilal Oswal Financial Services Ltd

Soft top-line performance; healthy margin delivery

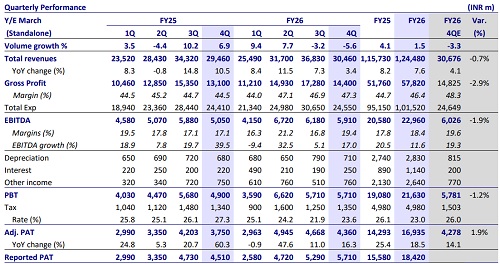

* United Spirits’ (UNSP) revenue grew 3% YoY to INR30.5b (in line) in 4QFY26. We were expecting weak revenue growth, given the policy change impact in Maharashtra and the high base of AP. Overall, volumes contracted 6% (vs. est. -3%, -3% in 3QFY26). The Prestige & Above (P&A) segment recorded 3% YoY decline in volumes (est. -1%), while it recorded value growth of 5%. The Popular segment reported 16% and 13% volume and revenue contraction YoY. Excluding Maharashtra and AP, revenue grew 9%.

* Gross margin expanded 280bp YoY to 47.3%, supported by headline pricing, product mix, and relatively stable input costs. Consequently, EBITDA margin expanded 230bp YoY to 19.4% (in line). Ongoing geopolitical tensions are expected to lead to ~5% increase in packaging costs in 1QFY27, which could impact gross margins by ~125–150bp; however, ~50% of the impact is expected to be offset by pricing actions, and the balance through productivity initiatives. Management reiterated its mid-to-high teen EBITDA margin guidance, and we model EBITDA margins of 18.7%/18.9% for FY27/FY28.

* Management indicated early signs of demand recovery and expects double-digit growth in the P&A portfolio during FY27. Recent policy changes in Karnataka (6–7% of revenue) are expected to drive high double-digit growth in the state. However, near-term disruption related to MML remains a key monitorable. Following the divestment of the RCB business, management aims to sharpen its focus on core alcoholic operations. We model revenue and EBITDA CAGR of 10%/11% over FY26-28E and reiterate our Neutral rating with a TP of INR1,500.

Highlights from the management commentary

* The India-UK FTA is expected to result in a high single-digit consumer price reduction for Scotch, with a 4% to 5% impact on the BIO portfolio.

* Karnataka is 6.5% of UNSP’s mix. The new Karnataka policy is progressive, and UNSP has seen price reduction in the range of 15-35% in P&A. Popular is expected to witness a price increase of ~17%.

* The A&P spend is expected to sustain at around 10.5% of net sales.

* The India-UK FTA is expected to result in a high single-digit consumer price reduction for Scotch, with a 4% to 5% impact on the BIO portfolio

Valuation and view

* We broadly maintain our estimates for FY26-FY28E.

* While Maharashtra and AP weighed on 4Q performance, UNSP delivered healthy performance in rest of India. Maharashtra contributes a mid- to highteen share of the company’s total revenue. USNP is taking various initiatives, such as improved packaging, pocket packs, and aggressive pricing to counter MML brands. In the coming quarters, we will continue to closely monitor the MML category and developments in the space.

* Management indicated early signs of demand recovery and expects double-digit growth in the P&A portfolio during FY27. Recent policy changes in Karnataka (6– 7% of revenue) are expected to drive high double-digit growth in the state.

* Following the divestment of the RCB business, management will sharpen its focus on core alcoholic operations. We model revenue and EBITDA CAGR of 10%/11% over FY26–28E and reiterate our Neutral rating with a TP of INR1,500.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412