Neutral United Spirits Ltd for the Target Rs.1,500 by Motilal Oswal Financial Services Ltd

Soft volume performance; heavy A&P spending dents margin

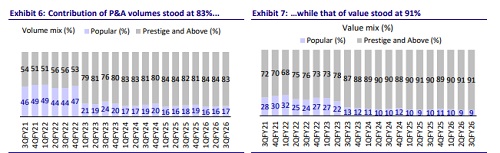

* United Spirits’ (UNSP) revenue grew 7% YoY (in line) in 3QFY26. Total volume declined 3% YoY (vs. est. +2% | +8% in 2QFY26). We expected a volume decline given the policy change impact in Maharashtra and heavy base due to AP (6% additional growth in base quarter). The Prestige & Above (P&A) segment volume fell 2% YoY (est. +2.5%), while value growth stood at 8% YoY. Popular segment reported a decline of 9%/5% in volume/revenue YoY.

* Gross margin expanded by 220bp YoY to 46.9% (est. 45.8%), supported by headline pricing, product mix and relatively stable input costs. High A&P spends (+36% YoY) dented profitability, resulting in a 30bp YoY contraction in EBITDA margin to 16.8% (miss). Management has reiterated confidence in sustaining its historical price mix range of 6-8%, which should help keep GM broadly stable despite inflationary pressure in bulk Scotch prices.

* The evolving trends in Maharashtra due to Maharashtra-made liquor (MML) will be a key monitorable as it is denting the growth pickup in other states. Gross margin has been expanding, aided by strong realization growth. We believe overall EBITDA margin will remain around 18.5-19.0%. Management is seeing early signs of consumption recovery but remains cautiously optimistic in the coming quarters. We broadly maintain our estimates for FY26-FY28E. We value UNSP at 45x Dec’27E standalone EPS and an additional INR250/share for RCB and other non-core assets to derive a TP of INR1,500. Maintain Neutral rating.

Weak volume growth; miss in EBITDA margins

* In-line sales, volume below expectation: Standalone net sales rose 7% YoY to INR36.8b (est. INR36.7b) in 3QFY26. P&A revenue (90% revenue mix) was up 8% YoY, while popular revenue fell by 5% YoY. The top half of the portfolio delivered a solid performance, which was partly offset by policyled headwinds in Maharashtra and the impact of one-time retail pipeline fill in AP in the base (15% growth in 3QFY25). Total volume declined by 3% YoY (est. +2% YoY, 8% in 2QFY26), with P&A volume down 2% YoY (est. +2.5% YoY, 8% in 2QFY26) to 14.6m cases. Excl. AP, P&A volume growth was flat YoY. Excl. Maharashtra, P&A volume grew by 6%, implying healthy growth in the rest of India. P&A revenue growth (excl. AP) stood at ~10% and excl. Maharashtra, it was 14%. Popular volume fell 9% YoY (est. +2% YoY, 6% in 2QFY26) to 2.9m cases due to MML impact.

* Taking initiatives to counter MML: MML achieved full distribution from Nov’25 onward, with availability steadily improving across brands. Management noted that the first brand to market has seen stronger consumer acceptance, while subsequent entrants have faced lower traction. Consumers continue to choose MML due to attractive pricing and value advantage. To counter MML, UNSP has doubled down on McDowell’s and Royal Challenge through improved packaging, sharper pricing, and the rollout of pocket packs.

* Higher A&P spends dent margins: Gross margin continued to expand by 220bp YoY to 46.9% (est. 45.8%, 47.1% in 2Q). Headline pricing, product mix and benign RM inflation have been supporting margin expansion. UNSP stated that bulk scotch prices started rising in Nov’25 and are expected to remain in inflationary mode for the next couple of quarters. Bulk Scotch is sourced from Diageo on a cost-plus model. A&P spends rose 36%, other expenses were up 7%, and employee expenses were flat YoY. Owing to high A&P spending, EBITDA margin was down by 30bp YoY at 16.8% (est. 17.8%). EBITDA was up 5% YoY at INR6.2b (est. INR6.5b).

* Flat PBT performance: Other income in standalone was INR1,440m, out of which INR510m was recurring (showing in consolidated P&L) and the rest was one-time dividend from subsidiary. We are considering only INR510m for PBT and the rest is in an exceptional item. PBT was flat YoY at INR5.7b (est. INR6.3b). A lower tax rate (22% vs. 26% last year) resulted in 11% YoY growth in APAT to INR4.7b (est. INR4.6b).

* In 9MFY26, net sales, EBITDA and APAT grew by 9%, 10% and 19%.

Highlights from the management commentary

* At a macro level, the company is witnessing consumption green shoots, with the top end of the portfolio delivering strong performance in 3Q. ? However, citing concerns about the job market and geopolitical volatility, management remains cautiously optimistic about the upcoming wedding season and the next couple of quarters.

* Launch of MML at attractive price points and gradual distribution increase remain a competitive challenge in Maharashtra, especially for the popular and lower-prestige segment (lower end of the portfolio).

* The India-UK FTA will be tabled in the British Parliament in Mar’26 or Apr’26. In India, the cabinet approval will be required. UNSP expects the implementation of FTA in 2QFY27.

* Key input costs remained benign, while bulk Scotch remained structurally inflationary (Nov’25 onward). UNSP expects bulk Scotch to remain inflationary for the next couple of quarters.

Valuation and view

* We broadly maintain our estimates for FY26-FY28E.

* While Maharashtra and AP weighed on 3Q performance, UNSP delivered healthy performance in the rest of India. Maharashtra contributes a mid- to high-teen share of the company’s total revenue. USNP is taking various initiatives such as improved packaging, pocket packs, and aggressive pricing to counter MML brands. In the coming quarters, we will closely monitor the MML category and developments in the space. On the margin front, a higher price mix range (6-8%) is expected to negate the adverse impact of inflationary bulk Scotch prices and higher ad spends.

* We value 45x Dec’27E standalone EPS and an additional INR250/share for its RCB and other non-core assets to derive a TP of INR1,500. Maintain Neutral rating

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

600-400.jpg)