Buy LatentView Analytics Limited for the Target Rs 480 by ARETE Securities Ltd

.jpg)

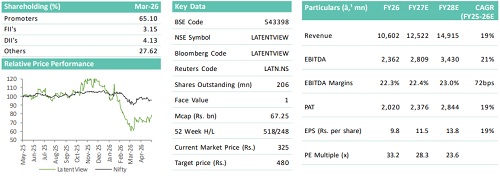

LatentView Analytics delivered a healthy performance in 4QFY26, with revenue at Rs 2,886 mn (+24.3% YoY / +3.8% QoQ), driven by continued strength in the BFSI and Consumer verticals despite ongoing headwinds in certain large technology accounts. Adjusted EBITDA stood at Rs 695 mn (+22.3% YoY / +8.5% QoQ), with margins remaining robust at 24.1%, reflecting strong operating leverage even as the company continued to invest in AI capabilities, Databricks partnerships, leadership hiring, and go-to-market expansion. PAT came in at Rs 551 mn (+7.4% YoY / +8.5% QoQ), supported by operational strength though partially impacted by higher investments and lower other income. FY26 revenue crossed the Rs 10 bn milestone, marking a significant achievement with ~28% CAGR since IPO. Strategically, the company continued to strengthen its positioning as an AI-led analytics and data engineering player, with ~49% of FY26 revenues coming from AI projects. During the quarter, LatentView expanded its Agentic AI and GenAI capabilities, deepened its partnership with Databricks by attaining Gold Partner status, and made a strategic $3 mn investment in Healtheon AI to build healthcare-focused AI orchestration capabilities.

Key Management Highlights-

• AI-led execution now contributes to nearly half of revenue, with growing traction in agentic AI, Databricks partnerships, and healthcare automation initiatives.

• The company is reducing dependence on large tech clients and the US market through strong BFSI growth, consumer vertical expansion, and wider geographic diversification.

• Management targets ~18–20% organic FY27 revenue growth, supported by AI-driven demand, BFSI momentum, and recovery in key technology accounts, while EBITDA margins are expected to remain around current levels.

Outlook and Valuation

LatentView Analytics continues to command a premium valuation, supported by its strong positioning in AI-led analytics, expanding GenAI and Agentic AI capabilities, and robust execution across BFSI and Consumer verticals. The company is increasingly evolving into an enterprise AI transformation partner, with ~28% of FY26 revenues linked to AI-led projects and nearly half of overall work involving AI in some form. Its strategic partnership with Databricks, growing traction in data engineering and cloud modernization, and recent $3 mn investment in Healtheon AI further strengthen its long-term growth outlook.

While continued investments in AI capabilities and GTM expansion may moderate near-term margin expansion, we expect Revenue/ EBITDA/PAT CAGR of ~19%/~20%/~18% over FY26-28E, driven by strong AI demand, BFSI momentum, and improving diversification. We maintain BUY, valuing the stock at 35x March-28E EPS of Rs 13.8, reflecting its premium positioning in the high-growth AI and analytics space and arrive at a target price of Rs 480. Maintain BUY.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127

.jpg)