Buy Kirloskar Oil Engines Ltd for the Target Rs.1,900 by Motilal Oswal Financial Services Ltd

Continued outperformance on revenue

Kirloskar Oil Engines (KOEL)’s 4QFY26 revenue outperformed once again with sharp growth in the powergen and industrial segments. KOEL has gained market share during FY26, with overall powergen market volumes growing 18% YoY. The company’s volume jumped 41% YoY in FY26. It has also gained near-double-digit market share in the HHP segment. The company has also announced an incremental capex of INR14b for expanding the capacity of engines. Going ahead, we expect KOEL to benefit from 1) incremental gains in both non-HHP and HHP powergen markets, 2) operating leverage benefits that can start playing out from FY27, 3) warranty renewal in the distribution segment, and 4) growth in the industrial segment. We expect exports to remain a bit patchy in the near term due to KOEL’s exposure to the Middle East. We revise our estimates by 5%/6% for FY27/28 and roll forward to Jun’28 estimates. We reiterate our BUY rating with a revised SoTP-based TP of INR1,900 (vs. INR1,600), valuing the core business at a slightly higher multiple of 30x to factor in strong growth across segments

Strong performance was in line with our expectations

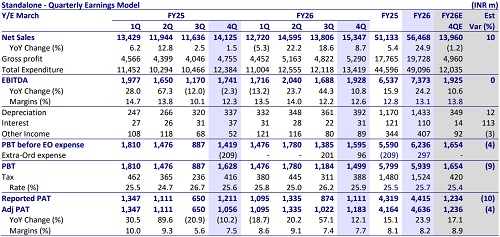

The company completed the transfer of its B2C segment to its wholly owned subsidiary through a slump sale. As a result, YoY growth rates are not comparable. On restated financials, revenue grew 24% YoY to INR15.3b, 10% above our estimate. Gross margin was broadly flat YoY at ~34.5% vs. our estimate of 35.5%. Absolute EBITDA increased 27% YoY to INR1.9b, in-line with our estimate, while margins expanded 30bp YoY to 12.6%. The margin was lower than our estimate, mainly due to higher-than-expected other expenses. Adj PAT increased 29% YoY to INR1.2b, broadly in line with our estimate. For FY26, revenue/EBITDA/PAT on revised financials increased 25%/24%/24% YoY, while EBITDA margin was flat at 13.1%. OCF increased 5% YoY to INR5b due to a better working capital position, while FCF declined 21% YoY to INR2b due to higher capex incurred in FY26.

Capex plans focused on high-value applications

The company announced a major capex program of ~INR14b at the Kagal facility over the next two years, focused on the HHP segment and export-oriented opportunities. This follows the earlier INR7b investment announced for adding 50,000 engine capacity, which is expected to come online by Apr’28. Unlike the earlier brownfield line expansion, the latest investment includes new buildings, fresh manufacturing lines, and infrastructure for larger and more sophisticated engines. The latest capex is targeted toward adding around 20,000 engines and reflects a strategic shift toward premium applications such as data centers, exports, nuclear, and critical infrastructure. Expected asset turnover of around 4x-5x indicates healthy utilization expectations and confidence in medium-term demand

Financial outlook

We raise our estimates by 5%/6% for FY27/FY28 and thus expect a revenue CAGR of 21% over FY26-28, driven by 22%/25%/15%/17% CAGR in powergen/industrial/ distribution/exports. Over FY26-28E, we bake in a 140bp improvement in margins to build in better product mix and operating leverage benefits. We expect an EBITDA/PAT CAGR of 27%/30% over the same period.

Valuation and recommendation

The stock is currently trading at 37.5x/29.6x P/E on FY27/28E earnings. Adjusted for subsidiary valuation, KOEL is trading at 33.6x/26.6x P/E on FY27/FY28E earnings, which is still at a significant discount to the market leader. We reiterate our BUY rating with a revised SoTP-based TP of INR1,900 (vs. INR1,600), valuing the core business at a slightly higher multiple of 30x to factor in strong growth across segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412