Buy EPL Ltd for the Target Rs.290 by Motilal Oswal Financial Services Ltd

Growth across all regions In-line operating performance

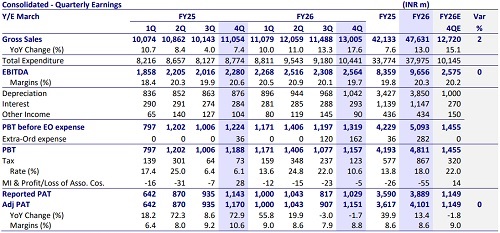

* EPL reported revenue of INR13b (up 18% YoY) in 4QFY26, driven by revenue growth across all geographies. The EAP posted the highest growth of 25% YoY on the back of strong performance in China. Americas/EU/AMESA delivered 24%/15%/10% YoY growth, with strong growth of ~28% YoY in Beauty & Cosmetics (BNC) and healthy growth in oral care of 10% YoY.

* We believe EPL is well-positioned to sustain its double-digit revenue growth trajectory, driven by continued BNC scale-up, recovery in oral care, emerging market expansion, and market share gains, while we expect gradual margin expansion to continue, supported by improved pricing discipline, operating leverage, and a higher BNC mix (40% of revenue in FY26 vs. 37% in FY25).

* We maintain our estimates for FY27/28 and value the stock at 15x FY28E EPS to arrive at our TP of INR290. Reiterate BUY.

Strong revenue growth; margins hurt by weakness in Europe

* Consolidated revenue grew 18% YoY to INR13b (est. in line). Gross margin stood at 59% (up ~100bp YoY). EBITDA margins contracted ~90bp YoY to 19.7% (est. 20.2%). EBITDA stood at INR2.6b (est. in line), up 13% YoY.

* Adj. PAT declined 2% YoY to INR1.2b (in line), led by lower other income than last year (adjusted for the impact of the proposed merger of INR156m)

* Revenue from AMESA/EAP/Americas/Europe grew 10%/25%/24%/15% YoY to INR3.9b/INR3b/INR3.8b/INR3.1b.

* EBITDA margins for EAP/Americas expanded 180bp/170bp to 21.4%/21.7%, whereas AMESA/Europe’s EBITDA margins contracted 160bp/300bp to 17.4%/14.2%.

* EBITDA for AMESA/EAP/Americas grew 1%/37%/42% YoY to INR683m/ INR647m/INR820m, whereas Europe EBITDA declined 5% to INR443m during the quarter.

* For FY26, EPL’s revenue/EBITDA/adj PAT grew 13%/16%/15% YoY to INR47.6b/INR9.7b/INR4.2b.

* The CFO for the year declined 9% to INR7.2b. Net debt stood at INR5b vs. INR4.5b as of Mar’25.

Valuation and view

* EPL continues to deliver a healthy operating performance across geographies (except Europe), supported by healthy demand, product innovations, an improving sustainable tube mix (38% of total volume in FY26 vs. 33% in FY25), and continued capacity expansion.

* With a focus on improving market share across geographies in the BNC segment and an expected recovery in Europe, we expect a CAGR of 8%/9%/16% in revenue/EBITDA/adjusted PAT over FY26-28. We value the stock at 15x FY28E EPS to arrive at our TP of INR290. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412