Buy Signatureglobal (India) Ltd for the Target Rs.1,030 by Motilal Oswal Financial Services Ltd

Upcoming launches key to support presales Presales to clock 13% CAGR during FY26-28E

SIGNATUR’s presales slightly declined by 3% YoY to INR15.7b in 4QFY26, but came in line with our estimate. Overall, FY26 presales declined by 20% YoY to INR83b, lower than its revised guidance. Two premium projects were launched in FY26 – Cloverdale in 1QFY26 and Sarvam in 3QFY26, which supported the operational performance. The forthcoming projects comprise a 19.8msf saleable area to be launched in the next 2-3 years. The company has planned launches worth INR150b and has guided for presales of INR100b in FY27. We expect 13% CAGR in pre-sales to INR105b during FY26-28E.

Project additions progressing well; enters JV for commercial development

In FY27, SIGNATUR added 2.3msf of projects in Sohna region as part of business development. Further, it entered into a license agreement with Tonino Lamborghini for the development of 812 branded residences in its premium residential project in Sector 71, Gurugram. The company has formed a strategic 50:50 JV with the RMZ Group, enabling its entry into the build-to-lease model over ~5.6msf leasable/saleable area. This would include a mix of office (4-4.5msf) and retail + hotels, which would generate annuity income once operational. It has envisaged a capex of INR35-40b for the annuity portfolio.

Proceeds from JV transaction led to significant deleveraging

Collections declined 22% YoY to INR9.1b in 4QFY26 and fell 8% YoY to INR40b in FY26. Considering a pickup in construction and presales growth, the company has guided for 25% YoY growth in collections to INR50b in FY27. We expect a 17% CAGR in collections to INR55b during FY26-28E. Net debt declined from INR10b in 3QFY26 to INR2b in 4QFY26 ( INR9b in FY25). This was mainly aided by proceeds of INR11.6b from the JV transaction with the RMZ Group. Factoring in cash inflows and capex requirement for the annuity portfolio, we expect net debt at INR3.6b/INR4.0b in FY27/FY28.

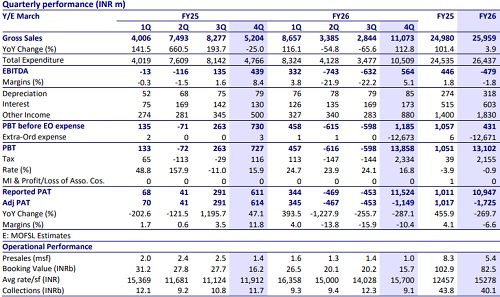

Financial performance

* In 4QFY26, revenue grew by 113% YoY to INR11b. EBITDA rose 29% YoY to INR564m with EBITDA margin at 5.1%. Reported PAT jumped ~18x YoY to INR11.5b on account of exceptional gains worth INR12.7b. PBT increased by 63% YoY to INR1.2b.

* In FY26, revenue grew by 4% YoY to INR26b. EBITDA loss stood at INR479m. Reported PAT surged ~10x YoY to ~INR11b on account of exceptional gains worth INR12.7b. PBT declined by 59% YoY to INR430m

Valuation and view

* SIGNATUR missed its revised FY26 presales guidance of INR100b. While the company has a concentrated exposure to the NCR market, it has a substantial launch pipeline during FY27-29. However, we will remain watchful of the pickup in operational performance in the coming quarters.

* We have valued the current residential portfolio on the DCF basis for the current portfolio (ongoing and forthcoming).

* We reiterate BUY rating with a TP of INR1,030, indicating a 17% upside potentia

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412