Neutral LIC Housing Finance Ltd for the Target Rs.630 by Motilal Oswal Financial Services Ltd

High repayments weigh on loan growth; credit costs benign Making efforts to accelerate disbursements and stem BT-OUTs

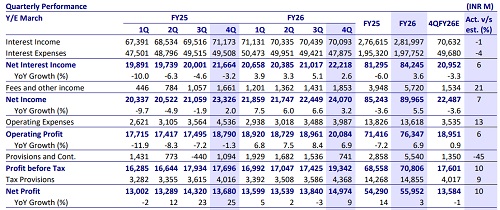

* LIC Housing Finance’s (LICHF) 4QFY26 PAT grew ~9% YoY to ~INR15b (~10% beat). FY26 PAT rose 3% YoY to ~INR56b. 4Q NII grew ~3% YoY to ~INR22.2b (~6% beat). Fee and other income grew 12% YoY to INR1.9b.

* Opex declined ~12% YoY to INR4b (~13% above est.) and cost-income ratio declined ~3pp YoY to ~16.6% (PY: ~19.4% and PQ: ~15.5%). PPoP grew ~7% YoY to ~INR20b (~6% beat).

* Credit costs stood at ~INR740m (vs. est. INR1.4b), translating into annualized credit costs of ~9bp (PY: 14bp and PQ: 20bp).

* LICHF’s growth is expected to be driven by a calibrated expansion strategy, supported by improvement of non-housing in the loan mix, deeper distribution reach, and improved operational efficiency. Management guided for loan growth of ~10-12% in FY27, supported by stronger disbursement momentum and improved sourcing through co-lending, DA structures, and partnerships with business aggregators.

* The introduction of a dedicated affordable housing vertical, along with a strong focus on LAP and LRD products, is expected to improve product mix and yield profile. Further support is likely to come from higher customer retention initiatives, and technology-led straight-through processing (STP).

* LICHF guided for FY27 NIM of 2.5-2.7%. Over the medium term, margin support is expected from a gradual portfolio shift toward higher-yielding LAP and LRD segments (mix improving from ~12% in FY25 to ~15% in FY26), which are being steadily scaled up and are likely to contribute to yield expansion.

* LICHF reported a healthy sequential acceleration in disbursements, though overall loan growth remained muted (up ~4% YoY) due to high repayments. Management remains optimistic about FY27, expecting seasonally stronger trends, supported by a recovery in disbursement momentum. NIMs are likely to remain stable, as the company continues to prioritize margin protection over aggressive growth. Asset quality remains steady and is expected to improve further, aided by recoveries, ARC sales, and continued resolution of stressed wholesale loans.

* We estimate a CAGR of ~8%/6% in advances/PAT over FY26-28E and RoA/RoE of 1.7%/13% by FY28E. With no near-term catalyst, we reiterate our Neutral rating on the stock with a TP of INR630 (based on 0.7x FY28E P/BV

Highlights from the management commentary

* LICHF has historically focused on organic sourcing of housing loans; however, it has now finalized its co-lending and direct assignment policies, which will support incremental growth. The company is also engaging with large business aggregators such as Andromeda to strengthen sourcing capabilities and expects this channel to contribute meaningfully to incremental volumes (~INR40-50b worth of business expected in the first year).

* A dedicated affordable housing vertical will be established with exclusive sourcing, underwriting, collections and recovery teams.

Valuation and view

* LICHF will have to navigate a competitive and uncertain macro environment with measured steps rather than sharp acceleration. While growth recovery, margin stability, and asset quality improvement are gradually building, external pressures and structural competition from banks may continue to weigh on near-term performance, leading to a more gradual earnings trajectory.

* LICHF’s valuation of ~0.7x FY27E P/BV reflects the inability of the franchise to deliver a respectable double-digit loan growth. We estimate a CAGR of ~8%/6% in advances/PAT over FY26-28E and RoA/RoE of 1.7%/13% by FY28E. With no near-term catalysts, we reiterate our Neutral rating on the stock with a TP of INR630 (based on 0.7x FY28E P/BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412