Buy Kaynes Technologies Ltd for the Target Rs.4,000 by Motilal Oswal Financial Services Ltd

Slower execution and sales deferrals lead to muted performance

Big miss on operating performance

* Kaynes Technologies (KAYNES) reported a lower-than-expected operating performance in 4QFY26, with EBITDA growth of 15% YoY (est. 49%). This was largely led by geopolitical disruptions, deferment of customer orders, delays in government projects, and a decline in revenue from a key EV customer.

* However, management emphasized that underlying industry demand, order book quality, and long-term growth prospects remain intact, with some revenue recognition shifting to future periods. Accordingly, management has guided for FY27 growth at nearly twice the industry growth rate (implying ~30% growth in FY27).

* While cash flow generation has been underwater due to higher receivables from the smart metering business, management has guided for faster installation in smart meters, shifting to a meter supply-only model and selling only to EPC/SPV partners.

* Factoring in lower-than-estimated earnings in 4Q and slower OSAT & PCB ramp up, we reduce our FY27/FY28 earnings estimate by 24%/17% and reiterate our BUY rating on the stock with a TP of INR4,000 (premised on 30x FY28E EPS)

Weak 4QFY26 performance; working capital elevated

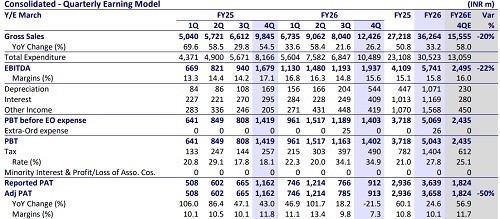

* Consolidated revenue grew 26% YoY to INR12.4b (est. INR15.5b) in 4QFY26, while EBITDA grew 15% YoY to INR1.9b (est. INR2.5b). EBITDA margin contracted 150bp YoY to 15.6% (est. 16%), led by a contraction in gross margin (down 40bp YoY) and an increase in employee expenses (up 260bp YoY), which was partly offset by other expenses (down 150bp YoY). Adj. PAT declined 22% YoY to INR913m (est. INR1.8b).

* Order inflows declined 65% YoY to INR5.3b in 4Q, with the order book growing 27% YoY. However, it declined 8% QoQ to INR84b

* Automotive/Industrials/Aerospace/Medical/ IT grew 46%/7%/4.4x/2%/81% YoY to INR3.3b/INR5.8b/INR439m/INR201m/INR2.1b, while Railways declined 22% YoY to INR507m.

* For FY26, Revenue/EBITDA/Adj PAT grew 33%/40%/24% to INR36b/INR5.7b/INR3.7b.

* For FY26, net working capital days increased to 125 from 87 days in FY25. Receivable days rose 50 days YoY, which was partially offset by payable days rising 18 days YoY. Net debt stood at ~INR2.1b vs. INR5.8b as of Mar’25.

* Gross debt stood at INR8.7b vs INR8.7b as of Mar’25. The company reported a cash outflow of INR6b vs INR823m as of Mar’25

Valuation and view

* KAYNES’ growth momentum slowed down in 4QFY26 due to geopolitical disruptions, deferment of customer orders, delays in government projects, and a decline in revenue from a key EV customer. However, with a healthy order book of ~INR84b as of Mar’26, the company is well positioned to recover and improve revenue growth momentum going forward.

* CFO remained under pressure (operating cash outflow of INR6b) due to elevated receivables in the smart metering business. However, it is likely to improve with faster meter installations and the transition of the smart metering business to a meter supply-only model, with focus on supplying to EPC/SPV partners.

* We estimate a revenue/EBITDA/adj. PAT CAGR of 42%/44%/55% over FY26- FY28. Reiterate BUY with a TP of INR4,000 (premised on 30x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412