Neutral Clean Science & Technology Ltd for the Target Rs.840 by Motilal Oswal Financial Services Ltd

Sequential recovery despite a challenging global environment Operating performance above our estimates

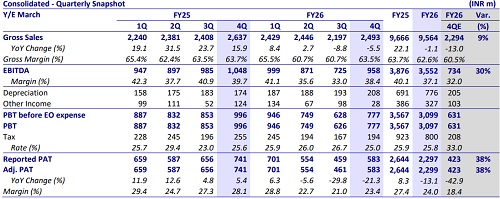

* Clean Science (CLEAN) reported an EBITDA of INR958m, down 9% YoY, while its gross margin dipped marginally to 63.5% (from 63.7% in 4QFY25). The EBITDA margin contracted to 38.4% (from ~39.7% in 4QFY25).

* FY26 was marked by a challenging global macro environment and geopolitical uncertainties, leading to subdued customer offtake and pricing pressure. We expect CLEAN’s earnings trajectory to move up due to its continued focus on process efficiency, backward integration, scale up of Hindered Amine Light Stabilizers(HALs), and the ramp up of performance chemical 1, along with the commercialization of performance chemical 2 in Sep’26E.

* We raise our earnings estimates for FY27/FY28 by 6% each and value the stock at 25x FY28E EPS to arrive at our TP of INR840. Reiterate Neutral.

Weak performance chemicals offset growth in pharma intermediates and FMCG

* The company reported a revenue of INR2.5b, down 5% YoY (est. INR2.3b), while revenue for Pharma & Agro Intermediates/FMCG Chemicals grew ~8%/~49% YoY to INR615m/INR366m. The revenue for performance chemicals (~61% of the revenue in 4Q) declined ~17% YoY to INR1.5b.

* Gross margin stood at 63.5% (compared to 63.7% in 4QFY25 ), while EBITDA margin stood at 38.4% (compared to 39.7% in 4QFY25)

* Employee exp as % sales stood at 2% (compared to 6% in 4QFY25) as the executive Directors voluntarily elected to forgo a substantial portion of their performance bonus entitlement for the FY25-FY26. Accordingly, the provision for performance bonus recognized in the earlier quarters has been reversed to that extent, resulting in lower employee benefits expense in 4Q.

* EBITDA declined 9% YoY to INR958m, above our estimate of INR734m. Based on the assumption of normalized employee costs (the average of the last three quarters), adj. EBITDA declined ~19% YoY to INR850m.

* Adj. PAT stood at INR583m (down 21% YoY) in 4QFY26 (est. INR423m).

* In FY26, revenue /EBITDA/Adj. PAT declined 1%/8%/13% to INR9.6b/ INR3.6b/INR2.3b

Valuation and view

* While the macro headwinds are expected to continue in the short term,

1) the ramp-up of the advanced grade HALs

2) strengthening HALs' presence in valueadded specialty chemistries

3) the scale-up of performance chemical 1 along with the commercialization of performance chemical 2

4) backward integration initiatives are expected to be key growth drivers going forward.

* We raise our earnings estimates for FY27/FY28 by 6% each and expect a CAGR of 21%/21%/25% in revenue/EBITDA/ PAT over FY26-28. We value the stock at 25x FY28E EPS to arrive at our TP of INR840. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412