Buy EPL Ltd for the Target Rs.280 by Motilal Oswal Financial Services Ltd

Margin expansions in Europe and the Americas drive profitability

In-line operating performance

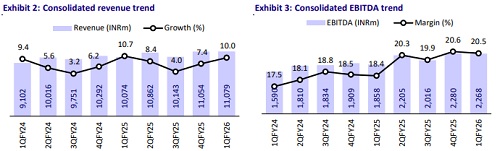

* EPL reported an EBITDA of INR2.3b (+22% YoY) in 1QFY26, in line with our estimate. This was driven by EBITDA growth across all regions, with Europe/America/EAP/AMESA witnessing a growth of 52%/35%/8%/2% YoY.

* EPL continued its trajectory of margin expansion (up 200bp YoY), supported by gains in Europe and the Americas. This was fueled by strategic restructuring, cost optimization, and an improving mix of the personal care segment in the overall portfolio (~54% in 1QFY26 vs. ~47% in 1QFY25).

* We maintain our estimates for FY26/FY27 and value the stock at 17x FY27E EPS to arrive at our TP of INR280. Reiterate BUY.

Product mix continues to improve and boost operating performance

* EPL’s revenue grew ~10% YoY to INR11b (in line). Gross margin expanded 70bp to 60%. EBITDA margin expanded 200bp YoY to 20.5% (est. 20.4%), led by improving margins in the Americas and Europe.

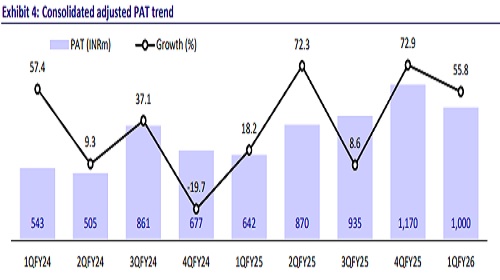

* The company’s EBITDA stood at INR2.2b (est. in line), up 22% YoY. Adj. PAT grew 56% YoY to INR1b (in line).

* Revenue from the Americas/Europe/EAP/AMESA grew 13%/15%/10%/2% YoY to INR2.9b/INR2.7b/INR2.6b/INR3.7b.

* EBITDA margin improved 300bp/400bp for the Americas/Europe to 18.8%/ 17.9%, while EBITDA margin for AMESA remained flat at 19%, and that of EAP contracted 30bp YoY to 21.6%.

* EBITDA for Americas/Europe/EAP/AMESA grew 35%/52%/8%/2% YoY to INR551m/INR478m/INR420m/INR714m during the quarter.

Highlights from the management commentary

* Guidance: EPL expects to maintain double-digit revenue growth, with EBITDA growth expected to be higher than revenue growth, driven by strong traction in the Beauty and Cosmetics (BNC) segment and the anticipated recovery in the oral care segment.

* Expansion: EPL has doubled its capacity in the BNC segment in Brazil, and this expansion is expected to enable the company to onboard new clients in the region. The Thailand plant is set to commercialize from 2HFY26.

* Personal care and beyond: Management is actively pursuing M&A opportunities in the BNC segment, targeting both geographic and product expansion. The growth momentum in the BNC segment is expected to continue, led by new customer additions due to capacity expansions.

Valuation and view

* EPL continues to deliver healthy operating performance across geographies, supported by a favorable product mix, product innovations, an improving sustainable mix (38% of total volume), and continued capacity expansion. We expect this positive trend to continue.

* With improved operational efficiencies, a focus on improving market share across geographies in the BNC segment, and a recovery in the Oral Care segment, we expect a CAGR of 9%/14%/22% in revenue/EBITDA/adjusted PAT over FY25-27. We value the stock at 17x FY27E EPS to arrive at our TP of INR280. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412