Buy JSW Steel Ltd for the Target Rs.1,520 by Motilal Oswal Financial Services Ltd

Earning beat; outlook remains bright Consolidated performance

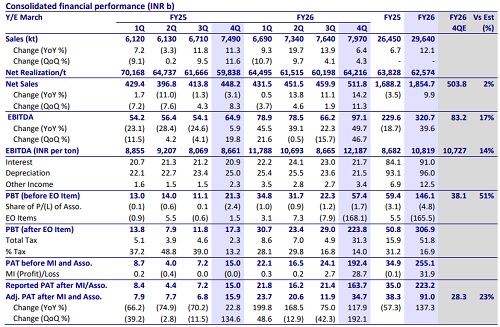

* JSW Steel (JSTL) posted in-line consolidated revenue of INR512b (+14% YoY and +11% QoQ) in 4QFY26, supported by healthy sales volume and NSR growth.

* Adj. EBITDA came in at INR97b, up 50% YoY and 47% QoQ, driven by higher sales realization, partly offset by higher coking coal prices. Adj. EBITDA/t stood at INR12,187, up 41% YoY and QoQ (vs. our est. of INR10,750/t).

* The company realized an exceptional gain of INR178.9b, which included INR181b related to the slump sale of BPSL steel undertaking and INR1.63b in exceptional charges on employee obligations arising from the implementation of the new labor code in 4Q, in addition to the charge taken in 3Q.

* APAT stood at INR34.7b (+117% YoY and +192% QoQ) against our est. of INR28.3b, mainly driven by better-than-expected operating performance.

* In FY26, revenue grew 10% YoY to INR1,855b, adj. EBITDA rose 40% YoY to INR321b, and APAT jumped 137% YoY to INR91b.

* Consol. crude steel production was down 2% YoY and flat QoQ at 7.5mt in 4QFY26 due to the shutdown of BF-3 in Vijayanagar for expansion. Steel sales volumes came in at 7.97mt (+6% YoY and +4% QoQ).

* ASP for the quarter stood at INR64,200/t (+7% YoY and QoQ), driven by steel price recovery on account of safeguard duty.

* In FY26, consol. production stood at 30.1mt (+8% YoY) and sales volume grew by 12% YoY to 29.6mt, while NSR declined 2% YoY to INR62,500/t on account of muted steel prices in 1H in the absence of safeguard duty.

* Net debt-to-EBITDA ratio stood at 1.81x in 4QFY26 vs. 2.91x in 3QFY26. Net debt as of Mar’26 stood at INR538.7b, down by INR264.8b QoQ, due to deleveraging from the slump sale of the BPSL steel business, healthy cash generation and the release of working capital.

India business performance – strong volume drives earnings

* Indian operation production for the quarter was 7.34mt, flat QoQ and down 1% YoY, due to Vijayanagar BF-3 shutdown for capacity upgrade since Sep’25, which impacted crude steel production and capacity utilization at the company's Indian operations during FY26.

* Steel sales for the quarter were at 7.84mt, up 6% QoQ and 8% YoY. Capacity utilization for the combined Indian operations for the year stood at ~92% ex-BF3 capacity (87% incl. BF-3 capacity).

* Indian operations registered revenue of INR487.7b (+14% YoY and +12% QoQ) and adj. EBITDA of INR95.7b (+47% YoY and QoQ), with an EBITDA margin of 19.6% during the quarter.

Valuation and view

* JSTL reported a strong performance in 4QFY26, supported by NSR improvement and sales volume growth. We believe JSTL is well-placed with new capacities coming on-stream, strong domestic demand, and a rising share of value-added proportion in the sales mix. Its focus on increasing the captive share of iron ore and improving coal linkages will support earnings.

* Going forward, we estimate double-digit revenue growth over FY27-FY28, driven by the ramp-up of new capacity and price recovery led by safeguard duty. Despite input cost volatility, we believe EBITDA/t will rebound to ~INR14,000/t by FY28E on account of domestic steel price recovery, led by safeguard duty.

* As BPSL was transferred to JFE JV via a slump sale, we have remodeled our FY27/28 earnings estimates excl. BPSL, which results in a decline in revenue and EBITDA by 9% in FY27. Our earnings estimates for FY28 decline by 3-4% to account for the BPSL business moving into a JV with 50% holding. At CMP, JSTL trades at 7.6x FY28E EV/EBITDA, and we reiterate our BUY rating on the stock with a TP of INR1,520, valued on SoTP

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412