Buy Lemon Tree Ltd for the Target Rs.160 by Motilal Oswal Financial Services Ltd

Renovation cycle nearing end; margins to expand

Lemon Tree Hotels (LEMONTRE) stands at a rare inflection point where years of deliberate, front-loaded investment in renovation, technology, and expansions are about to converge into a sustained margin improvement story.

* The company has strategically invested ~INR3b over FY23-FY26 (and ~INR1.3b is expected in FY27) in a phased renovation cycle (major part) and technology transformation.

* These investments have temporarily compressed the EBITDA margin from its FY23 peak of ~52% to ~49% in FY24 and ~49.4% in FY25. As these investments are expected to largely be completed by the end of FY27, the stage is set for a significant margin re-rating in FY28 and beyond.

* Encouragingly, renovation is already delivering measurable on-the-ground results. Delhi RevPAR grew 11% YoY despite 100 rooms offline; Hyderabad RevPAR rose 19% despite 60 rooms under renovation.

* Beyond renovation, LEMONTRE is simultaneously building a focused Aurikabranded owned portfolio — Shimla (91 keys, 2QFY27 opening), Shillong (first hospitality PPP with the Meghalaya government; ~INR2b investment at an effective debt rate of ~2.5-3.0%), Varanasi heritage (47 keys on the ghats; ARR economics equivalent to a 150-room Aurika), and Nehru Place, Delhi (~550 rooms with construction commencing in 2–3 months). At peak potential, these properties are expected to contribute 25% of FY28 revenue and ~30% of FY28 EBITDA at superior margins.

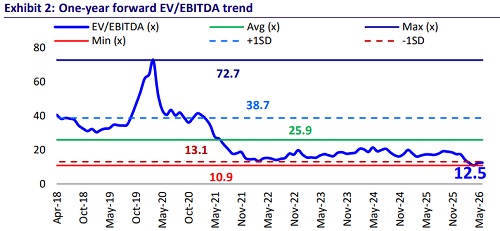

* We expect LEMONTRE to report a CAGR of 11%/15%/24% in revenue/EBITDA/ PAT over FY26-28. We value the stock with our SOTP-based TP of INR160. Reiterate BUY.

Heavy lifting on margins nearing the end

* Over the past two years, Lemon Tree Hotels has pursued a multidimensional investment strategy encompassing physical asset renovation, digital transformation, human capital build-up, and new property construction.

* These investments were deliberate and front-loaded and were aimed at repositioning the portfolio for a higher-margin, higher-ADR future. The combined effect has temporarily suppressed margins, but management has consistently guided that the payback window is two years due to operating investments.

* LEMONTRE has strategically invested ~INR3b over FY23–FY26 in a phased renovation cycle, technology transformation, and human capital expansion. These investments have temporarily compressed the EBITDA margin from its FY23 peak of ~52% to ~48% in FY26E.

* The company, as of FY26, has renovated ~3,000 rooms (translating into a per-room renovation cost of ~INR1m). Of the total renovation expense of ~INR3b, opex is ~INR1.4b, which directly affects its margins, while the balance is the capex portion. The company is expected to complete its last leg of renovation in FY27 with an expected outflow of ~INR1.3b (~40-45% will be opex) in FY27 for renovating the balance of ~1,200 rooms

* Further, to align its operations with the new age, tech-savvy customers, the company has been investing in technology upgrades in consultation with BCG. Some key initiatives have been an AI-driven revenue management program, sales platform overhaul, loyalty program relaunch, cybersecurity, and operational tech upgrades. Over the last two years, the company has spent ~INR150m (i.e., ~0.5-0.6% of total revenue), and the expenditure is likely to continue in the coming years.

* As the majority of these investments (largely renovation) are expected to be completed by FY27, the stage is set for a significant margin re-rating in FY28 and beyond.

Valuation and view

* LEMONTRE enters FY27 with its significant investment cycle nearing completion, a record managed hotel pipeline (~9,364 keys under management/franchise contracts), and premium Aurika assets coming online (~850 keys greenfield).

* With renovation opex normalizing, technology investments yielding results, and management fees compounding at a healthy rate, EBITDA margins are poised to expand meaningfully from FY26E's ~48% toward 50-51% by FY28, supporting a strong 24% PAT CAGR over FY26–28.

* We expect LEMONTRE to report a CAGR of 11%/15%/24% in revenue/EBITDA/ PAT over FY26-28. We value the stock using the SoTP approach to arrive at our TP of INR160. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)