Buy Indian Hotels Ltd for the Target Rs.785 by Motilal Oswal Financial Services Ltd

Healthy operating performance driven by diversification and scale Operating performance in line with estimate

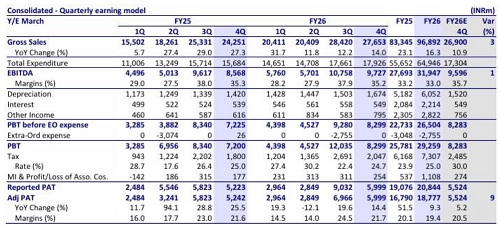

* Indian Hotels (IH) reported healthy consolidated revenue growth of 14% YoY in 4QFY26, led by 13% growth in standalone business and 16% growth in subsidiaries. Growth in standalone business was led by room revenue (up 12% YoY, ARR up 9%, OR up by 190bp), followed by F&B revenue (up 6%) and management fees (up 24% due to new signings).

* IH is expected to clock 12-14% growth in FY27, primarily driven by new asset additions (378 keys addition in Ekta Nagar and Varanasi), integration of newly acquired brands with expected revenue of INR2.5b in FY27 (Clarks, Brij, and Atmantan), RevPAR growth of 7-9%, and scale-up of new and reimagined brands. Moreover, the company has a pipeline of 31,300 keys (with 80% of the signed pipeline being asset-light) almost equal to its current operational keys of 33,091, thereby aiding higher profitability.

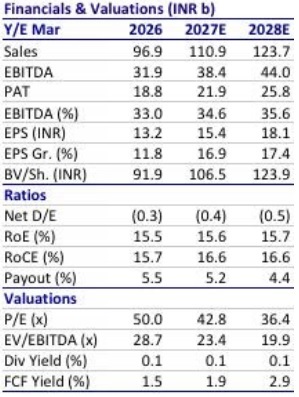

* We expect IH’s performance to continue its uptrend, with a CAGR of 13%/17%/17% in revenue/EBITDA/adj. PAT over FY26-28. We broadly maintain our FY27/FY28 EBITDA estimates and reiterate BUY with our SoTP-based TP of INR785.

Sustained growth momentum across businesses

* Revenue grew 14% YoY to INR27.6b (est. in line). Of this, Hotel segment/ Taj Sats grew by 14%/13% YoY to INR24.5b/INR3.2b.

* Standalone revenue/EBITDA rose 13%/17% YoY to INR16.6b/INR7.9b, aided by an increase in ARR (up 9% YoY to INR22,927), while OR expanded 200bp to 82%. F&B/other services/management fee income grew 6%/17%/25% YoY. * EBITDA grew 14% YoY to INR9.7b (est. in line). EBITDA margins declined by 15bp YoY to 35.2%. Adj. PAT grew 14% YoY to INR5.9b (est. INR5.5b).

* Subsidiary (cons. less standalone) sales at INR11.0b rose 16% YoY. Subsidiary EBIDTA came in at INR1.8b, up 1.2% YoY. TajSATS revenue/ EBITDA grew ~14%/7% YoY.

* UOH/St. James’ revenue grew 27%/21% YoY, while EBITDA fell 17%/14%.

* IH’s new business verticals, comprising Ginger, Qmin, and amã Stays & Trails, grew 25% YoY to INR7.5b in FY26.

* For FY26, revenue/EBITDA/adj PAT grew 16%/15%/12% to INR97b/ INR32b/INR9b. Gross debt stood at INR513m vs. INR2.2b as of Mar’25. CFO stood at INR25b vs. INR22b as of Mar’25.

Valuation and view

* IH’s growth outlook remains optimistic despite near-term geopolitical and macroeconomic uncertainties, led by healthy traction in the core business as well as new and reimagined businesses. This is also attributable to the expansion of brand-scape through the acquisition of niche category hotels.

* We expect the strong momentum to continue in the medium term, led by:

1) a strong room addition pipeline in owned/management hotels (6,400/24,900 rooms)

2) strategic acquisitions

3) continued favorable demand-supply dynamics

4) increasing MICE activities in India.

* We broadly maintain our FY27/FY28 EBITDA estimates and reiterate BUY with our SoTP-based TP of INR785.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412