Buy Coforge Ltd For Target Rs. 1,800 by Motilal Oswal Financial Services Ltd

A meaningful step-up

Margin profile sees a quantum jump despite near-term revenue snag

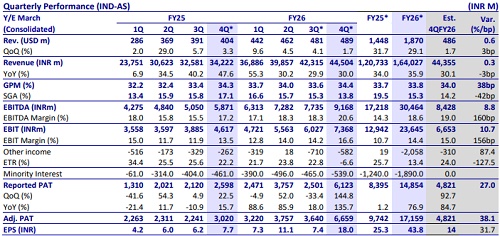

* COFORGE reported a strong 4Q revenue growth of 2% QoQ in CC terms, above our estimate of 1.5% QoQ CC. The company reported an order intake of USD648m (down 69.5% YoY) in 4Q with five large deals, resulting in a robust 12-month executable order book of USD1.75b. EBIT margin stood at 16.6%, above our estimate of 15%. Adj. PAT stood at INR6.6b (up 119% YoY) vs. our estimates of INR4.8b. The FCF-to-NI ratio stood at 76.3% in FY26.

* FY26 revenue/EBIT/adj. PAT grew 35.9%/82.7%/73.8% YoY. In 1QFY27, we expect revenue/EBIT/adj. PAT growth of 23.5%/57.3%/56.3% YoY in INR terms. RoE came in at 16.5% in FY26 (vs. 13.9%/24.1%/23.1% in FY25/FY24/FY23). We value COFORGE at 26x FY28E EPS, arriving at a TP of INR1,800, implying 54% potential upside.

Our view: Striving to be on the right side of the AI-wave

* Revenue restated, hedged loss/gain now part of other income (previously a part of operational revenue): This has no impact on PAT but revenue and EBIT margin numbers are now restated and they do not include the impact of hedge losses. For context, hedge losses had an 80bp impact on EBIT margin in FY26 (nil in FY25).

* Exiting the India pass-through business improves working capital as well as margin profile: Coforge's India government business was pass-through in nature, and it has decided to exit this business. On a full-year basis, this would have a hit of 2-3%; majority of the impact will flow through in 1QFY27 (which is expected to be flat QoQ). While this blunts short-term growth rates, the deal book remains strong (executable order book at USD1.75b, +16.4% YoY, with additional framework agreements not included) and we expect Coforge to grow after the reset in 1Q.

* EBIT margin guidance receives a meaningful upgrade: Even assuming a similar impact of hedge losses in FY27, the updated margin guidance is at least 100-150bp above our earlier estimates. This is a meaningful uplift; we increase our EPS estimates by 3-4% despite the one-time impact from the India business hit.

* Executable order book provides visibility into FY27: Deal momentum remained healthy in 4Q, with order intake of USD648m and five large deal wins, taking total large deal wins for FY26 to 21 (vs. 14 in FY25), ahead of management guidance of 20 deals. The executable order book stands at USD1.75b (up 16.4% YoY), providing revenue visibility into FY27.

* Coforge finding pockets of growth in AI: Demand is shifting from experimentation to production-grade deployments with a focus on agent orchestration, enterprise workflows and managed services around AI systems. We are positively surprised at the book's resilience to AI deflation, with management highlighting 25-35% productivity gains in development and 40-60% in code generation, yet sustained demand for maintenance, security and integration services.

? BFS uncharacteristically weak, management expects turnaround: Coforge's BFSI vertical has remained weak for the past couple of quarters (decline of 2.0%/2.6% QoQ in 3Q/4Q). A key leadership exit in the vertical has coincided with this; management expects the vertical to be back on track in FY27, supported by deal pipeline and re-engagement in key accounts (2 of 5 large deals in 4Q from banking).

Valuation and changes to our estimates

* We expect COFORGE to be the growth leader within our coverage universe and we reiterate it as our top pick. We have increased our estimates by 3-4% to factor in the exit of the India pass-through business (2-3% revenue impact) and the restatement of revenue (hedge impact now excluded from EBIT), while building in a 100-150bp improvement in margin guidance.

* We continue to view COFORGE as a structurally strong mid-tier player, supported by improving margin profile, strong deal wins, and steady demand in AI-led managed services. We value COFORGE at 26x FY28E EPS with a TP of INR1,800, implying a 54% potential upside. We reiterate our BUY rating on the stock.

Beat on revenue and margins; Deal TCV healthy with five large deal wins in 4Q; FCF/NI at 110%

* COFORGE’s revenue grew 2% QoQ CC (est. 1.5% CC). Reported USD growth was 1.7% QoQ. For FY26, revenue stood at USD1.9b, up 29.2% YoY.

* Growth was led by the Healthcare and Hi-Tech vertical (12% QoQ) and Transportation (4.5% QoQ), while BFS declined 2% QoQ.

* Order intake was USD648m (down 69.5% YoY). Five large deals were signed in 4Q. The 12-month executable order book rose 16.4% YoY to USD1.75b.

* Management expects to deliver robust revenue growth in FY27 and EBITDA of more than 20.5% on a consolidated basis in FY27.

* EBIT margin was 16.6%, above our estimates of 15%. For FY26, adj. EBIT margin stood at 14.4% vs. 10.5% in FY25.

* Utilization grew 80bp QoQ to 82.5%. Net employee addition stood at 35,777, up 1.2% QoQ. Attrition was down 10bp QoQ at 10.8%.

* Adj. PAT stood at INR6.6b (up 119% YoY) vs. our estimates of INR4.8b. For the full year, adj. PAT stood at INR17.9b, up 83% YoY.

* FCF/PAT stood at 110% in 4QFY26.

Key highlights from the management commentary

* Despite a challenging macro and heightened AI-driven flux, management maintains that demand tailwinds for Coforge are structural – the near-term modernization surge, the medium-term agentic deployment wave, and longterm tech market expansion all play to its strengths.

* Management addressed concerns around AI code deflation, noting that AIgenerated code is cheap to build but expensive to own, maintain, and secure, creating a recurring high-margin managed services opportunity for firms positioned to capture it.

* Demand remains broad-based, with all key verticals – travel, healthcare, banking, insurance, and public sector – firing simultaneously; management expressed confidence that growth does not depend on any single vertical.

* Framework agreements (not captured in the executable order book) have already been signed and are expected to contribute materially to FY27 revenue; management indicated that additional, larger framework agreements are at near-final stages of closure.

* Cross-selling momentum from prior acquisitions is evident. Clients acquired through the Cigniti deal, who previously contributed USD25-30m collectively, have now scaled up to ~USD75m/year. ? AI is deeply embedded across the SDLC: the firm reports 25-35% productivity uplift in development, 40-60% in code generation, and up to 10x faster modernization timelines.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412