Buy KEI Industries Ltd For Target Rs.5,780 by Motilal Oswal Financial Services Ltd

Earnings beat; Sanand ramp-up to drive growth ahead

Capacity-led growth to accelerate; margins to expand from FY28

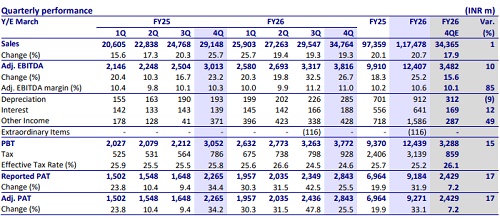

* KEI Industries (KEII)’s 4QFY26 revenue grew ~19% YoY to INR34.8b (in line). EBITDA increased ~27% YoY to INR3.8b (~10% beat, driven by higher-thanestimated margin in C&W). OPM rose 65bp YoY to 11% (+85bp vs. estimate). PAT grew ~25% YoY to INR2.8b (~17% beat).

* Management remains optimistic, guiding a strong volume growth of ~17- 18% in FY27 and ~20% in FY28, aided by strong capex momentum across key sectors and the ramp-up of its capacity expansion. However, volume growth in 4QFY26/FY26 at ~2%/~6% was modest, mainly due to capacity constraints and the slow ramp-up of Sanand (Phase 1) expansion. Its margin is likely to remain stable at ~10.5–11.0% in FY27, with further expansion from FY28 expected, backed by operating leverage, improved mix, and higher exports.

* We increase our EBITDA estimates by ~4%/7% for FY27/FY28 due to higher growth estimates in C&W. We also raise our EPS estimates by ~9%/12%, led by higher EBITDA and lower depreciation/higher other income estimates. We value KEII at 40x FY28E EPS to arrive at a TP of INR5,780. Reiterate BUY.

C&W revenue rises 18% YoY, and EBIT margin expands 1.5pp YoY to 12%

* KEII’s revenue/EBITDA/Adj. PAT stood at INR34.8b/INR3.8b/INR2.8b (+19%/ +27%/+25% YoY and +1%/+10%/+17% vs. our estimates) in 4QFY26. OPM expanded 65bp YoY to ~11%. Depreciation/interest costs rose ~47%/35% YoY. Other income increased ~15% YoY.

* Segmental highlights: a) C&W revenue was up ~18% YoY at INR33b, EBIT rose ~34% YoY to INR4.1b, and EBIT margin increased 1.5pp YoY to 12.0%. b) EPC business revenue remained flat YoY to INR2.2b, EBIT declined 72% YoY to INR47m, and EBIT margin dipped 5.5pp YoY to 2.1%. c) Stainless steel wire (SSW) revenue increased ~21% YoY to INR561m, EBIT surged to 2x YoY to INR50m, and EBIT margin jumped 3.5pp YoY at 8.9%.

* In FY26, revenue/EBITDA/adj. PAT grew 21%/25%/33% YoY to INR117.5b/ INR12.4b/INR9.3b. EBITDA margin surged 40bp YoY to 10.6%. C&W revenue/ EBIT rose 22%/33% YoY to INR112.2b/INR13.0b, and EBIT margin expanded 1.0pp YoY to 11.6% in FY26. OCF stood at INR8.4b vs. operating cash outflow at INR322m in FY25. Capex stood at INR11.3b vs. INR6.9b. Net cash outflow stood at INR2.9b vs. INR6.6b in FY25.

Key highlights from the management commentary

* KEII has confirmed that none of its plants have faced any disruptions due to raw material constraints, given an adequate inventory stocking and sufficient domestic availability. However, certain challenges persist on the logistics front, mainly in the Middle East.

* The company’s order book reported a healthy backlog, including INR6.25b in EHV cables, INR3.1b in EPC, INR21.5b in domestic institutional cables, and INR5b in export orders. Additionally, L1 orders in EHV cables were INR2.3b.

* Capex was pegged at INR6.0-7.0b p.a. for the next two to three years, towards capacity expansion, backward integration, and land acquisitions. This capex will be largely funded through internal accruals, with a disciplined allocation framework.

Valuation and view

* KEII reported a steady 4Q performance with strong traction in high-value segments, mainly EHV cables and robust B2C growth, which increased its share to ~56% vs. ~51% in 4QFY25. However, near-term growth will be partially constrained by capacity limitations at existing plants, which are already operating at near peak utilization. Incremental growth will therefore be driven primarily by new capacities. It is scaling up exports with a target of ~20% of total revenue in FY27 vs. ~16% in FY26.

* We estimate KEII’s total revenue CAGR at ~19% over FY26-28, led by ~20% growth in the C&W segment and ~3% growth in the SSW segment. However, EPC revenue is projected to decline by ~8% annually. We project its EBITDA/ PAT CAGR of ~24%/21% over FY26-28. The stock is trading at 43x/35x on FY27E/FY28E EPS. We value KEII at 40x FY28E EPS to arrive at our TP of INR5,780. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412