Neutral Indus Towers Ltd for the Target Rs. 430 by Motilal Oswal Financial Services Ltd

Slightly weaker 4Q; elevated capex weighs on FCF generation in FY26

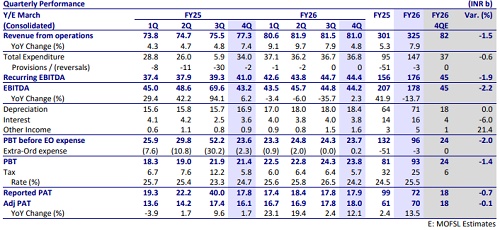

* Indus Towers’ (Indus) 4QFY26 was slightly weaker than our estimates, with recurring EBITDA (excl. provisions) declining 1% QoQ to INR44.3b.

* Operationally, tower additions picked up QoQ and tenancy additions remained steady. Management indicated that orderbook remains robust.

* Indus’ capex increased 18% QoQ (in line with tower additions). However, the QoQ lower receivables aided in improved FCF of INR11b in 4Q (vs. ~INR8b in 3Q).

* For FY26, Indus’ capex remained elevated at INR88.2b and weighed on FCF generation (~INR38b vs. INR98.5b in FY25, which was boosted by bad debt collections). The company reinstated dividends at INR14/share, which implies a payout of ~100% of FY26 FCF generation, while the company has retained FY25 FCF along with the collection of past dues for investments.

* A potential fundraise by Vi, following the recent AGR relief, could improve visibility on the commencement of INR450b capex plan, which would also potentially benefit Indus. We currently bake in ~30k/~50k tenancies/5G loadings from Vi over FY26-29, while we build in modest ~5k exits from RJio (~10% of its overall portfolio with Indus).

* Our FY27-28E estimates are broadly unchanged. We build in a CAGR of ~4-6% in Indus’ revenue/pre-IND AS EBITDA/adj. PAT over FY26-28E.

* We reiterate our Neutral rating with a revised DCF-based TP of INR430, premised on DCF-based 6.6x FY28E pre-IND AS EV/EBITDA. RJio’s tenancy risks cloud the potential benefits from Vi’s planned capex.

Slightly weaker 4Q; tower additions picked up, ARPT declined

* Tower additions picked up QoQ to 4.99k (vs. 3.55k in 3Q and our est. of 3.5k), while tenancy additions remained steady at ~6.2k (vs. 6.1k QoQ and our est. of 6k).

* Reported average revenue per tenant (ARPT) at INR41.1k (-2% YoY) declined 1% QoQ. The base quarter had certain one-off reconciliation benefits.

* Consolidated revenue moderated 0.6% QoQ to INR81b (+5% YoY), as service revenue grew 0.6% QoQ (+5.2% YoY), while energy reimbursements declined 2.8% QoQ (+4% YoY).

* Consolidated reported EBITDA declined 1% QoQ at INR44.2b (+2% YoY, 2.2% below), largely due to an increase in repairs and maintenance expenses.

* Adjusted service EBITDA at INR45.3b (flat QoQ, +7% YoY) was slightly below our estimate, largely due to weaker ARPT.

* Energy under-recovery was in line with our estimate at ~INR1b (vs. under-recovery of INR0.8b in 3Q and INR1.5b YoY).

* Indus reported a bad debt provision of INR153m in 4Q (vs. reversals of INR13m QoQ, our est. of NIL and INR2.3b YoY)

* Adjusted for provision reversals, recurring EBITDA at INR44.3b, declined 1% QoQ (+8% YoY) and below our estimate of INR45.2b

* Reported PAT at INR17.9b (stable QoQ and YoY) was broadly in line with our estimate. Adjusted PAT was also broadly in line with our estimate. ? FY26 revenue at INR325b grew 8% YoY, with service revenue at INR209b rising 9% YoY and energy reimbursement rising 6% YoY to INR192b.

* Reported FY26 EBITDA at INR178b declined ~14% YoY due to lower bad debt reversals. Adjusted for bad debt reversal of INR2.7b (vs. INR50.9b YoY), recurring EBITDA grew ~13% YoY to INR175b, driven largely by the acquisition of towers from Bharti Airtel in Mar’25.

* Indus added 15.2k net towers and ~22.6k net tenancy in FY26, with incremental tenancy ratio of 1.48x (1.62x on EoP basis).

Elevated capex continues, though receivables moderate QoQ

* With a pick-up in tower addition, capex surged 18% QoQ to ~INR23.3b. Maintenance capex remained elevated as the company continues to invest in energy efficiency initiatives such as solarization and battery replacement.

* Receivables declined ~INR3.7b QoQ to ~INR49.4b.

* Reported FCF came in at INR11b in 4Q (vs. INR7.9b in 3Q). ? For FY26, FCF remained muted at INR37.6b (vs. INR 98.5b in FY25, which was boosted by the collection of Vi’s past dues), due to elevated capex.

* Net cash (excluding leases) improved to ~INR49.3b (up ~INR15b QoQ).

Key highlights from the management commentary

* Elevated capex: Capex remains elevated, driven by tower additions, investments in energy efficiency initiatives, creation of additional infrastructure to support second tenants on existing towers, and continued maintenance capex for strengthening the aging tower portfolio and battery replacements. Management noted that 70-75% of the capex is directed towards driving growth and depends on the tower/tenancy additions, while maintenance capex could remain elevated over the next few years due to ongoing battery replacement.

* Shareholders’ returns: Given an improved visibility on business momentum and GoI’s continued support for Vi, Indus has reinstated dividends at INR14/share, equivalent to FY26 FCF generation. Management indicated that the company would follow a steady and progressive dividend policy after taking into account capex and other requirements, though it remained non-committal on paying out a collection of significant past dues from FY25.

* Orderbook: Indus continues to garner a high share in its key customers’ rollouts. Management indicated that the order book remains healthy, but it remains watchful of ongoing supply disruptions due to the West Asia conflict. The company has also been gaining share from other tower cos through migration by key customers, driven by Indus’ superior cost efficiency and network uptime track record.

Valuation and view

* A potential fundraise by Vi, following the recent AGR relief, could improve visibility on the commencement of INR450b capex plan, which would also benefit Indus.

* We currently bake in ~30k/~50k tenancies/5G loadings from Vi over FY26-29, while we build in modest ~5k exits from RJio (~10% of its overall portfolio with Indus).

* Our FY27-28E estimates are broadly unchanged. We build in a CAGR of ~4-6% in Indus’ revenue/pre-IND AS EBITDA/adj. PAT over FY26-28E.

* We reiterate our Neutral rating with a revised DCF-based TP of INR430 (earlier INR440), premised on DCF-based 6.6x FY28E pre-IND AS EV/EBITDA. RJio’s tenancy risks cloud the potential benefits from Vi’s planned capex.

* Indus’ elevated capex weighed on FY26 FCF generation and, thereby, dividend yield. A moderation in maintenance capex remains the key for improved FCF generation.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412