Neutral NALCO Ltd for the Target Rs. 400 by Motilal Oswal Financial Services Ltd

Revenue in line; cost inflation leads to profitability miss; favorable aluminum prices drive earnings revision

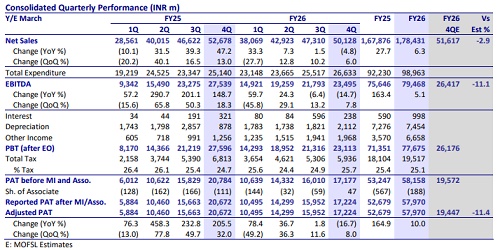

* NALCO’s (NACL) revenue stood in line at INR50.1b (-5% YoY and +6% QoQ), mainly driven by favorable aluminum prices.

* Consol EBITDA stood at INR23.5b (-15% YoY and +8% QoQ), against our est. of INR26.4b, during the quarter.

* EBITDA margin stood at 46.9% in 4QFY26 vs 46.1% in 3QFY26 and 52.3% in 4QFY25.

* Adj. PAT for the quarter stood at INR17.2b (-17% YoY and +8% QoQ) against our est. of INR19.5b, led by operating performance miss.

* In FY26, revenue stood at INR178b (+6% YoY), EBITDA at INR79.5b (+5% YoY), and APAT at INR58b (+10% YoY).

* The Board approved the third interim dividend of INR2 per share (~40% on FV) during the quarter.

Aluminum business

* Revenue from the aluminum business stood at INR39b, up 20% YoY and 13% QoQ on account of favorable LME prices.

* Metal production stood at 117kt, down 1% YoY and 3% QoQ, while sales volume was at 122kt, declining 3% YoY and QoQ during the quarter.

* ASP for aluminum stood at USD3,485/t, increasing 24% YoY and 16% QoQ, driven by favorable LME prices. ? EBIT stood at INR19b, up 32% YoY and 20% QoQ in 4QFY26.

Chemical (Alumina) business

* Revenue from the chemical business declined 38% YoY and 5% QoQ to INR15.7b, mainly due to a correction in global alumina prices.

* Alumina hydrate production stood flat QoQ at 574kt, down 2% YoY, while sales volume decline 1% YoY and 15% QoQ to 343kt.

* ASP for alumina hydrate remained flat QoQ at USD354/t (-47% YoY) due to a sharp correction in alumina prices from ~USD580/t to ~USD300/t over 12M.

* EBIT came in at INR4b, down 70% YoY and 23% QoQ in 4QFY26.

Key highlights from the management commentary

* Management targets ~200-250kt of volume in FY27E from the new refinery, with full ramp-up to be seen in FY28E.

* NACL’s domestic alumina sales rose from ~40kt in FY25 to 140kt in FY26, and in FY27, domestic sales are targeted at 250-300kt, reducing export dependence.

* Management expects 1QFY27 profits to remain strong, potentially sustaining quarterly PBT above INR20b, supported by elevated aluminum prices despite weaker alumina. While alumina profitability is expected to face headwinds, aluminum margins are expected to remain the primary earnings driver.

* Management expects continued pressure on alumina prices in FY27, with average realizations projected at ~USD300-USD310/t against USD376/t in FY26.

* Current aluminum prices range at USD3,500-3,600/t due to war-related disruptions and curtailed Middle Eastern smelter output. NACL expects average FY27 aluminum realizations to normalize to ~USD3,000-3,100/t if capacity in the Middle East comes online; however, prices will still be significantly above the FY26 average of ~USD2,674-2,700/t. Therefore, since aluminum contributes ~73% to NACL’s revenue, higher aluminum prices are expected to offset lower alumina profitability and support overall margins.

Valuation and view

* NACL posted a decent performance in 4Q, led by favorable aluminum prices and healthy volume, which helped offset the muted alumina price impact during the quarter. With limited production room at the smelter, LME prices have become a vital factor for near-term operating performance.

* The company has planned an expansion (total outlay of INR200-250b), which is expected to significantly enhance capacity in the long run. However, with the completion timeline of FY30, execution risks and cost escalations remain key concerns.

* Despite strong fundamentals, zero debt, favorable LME prices, and a robust demand outlook for aluminum in India, the near-term upside is capped by limited production headroom, geopolitical tension, on-time execution challenges, and regulatory risks.

* We raise our EBITDA/PAT estimates for FY27 by 9%/12% and 6%/8% for FY28, incorporating the favorable LME price benefits.

* At CMP, NACL trades at 7.5x on EV/EBITDA. We reiterate our Neutral rating on the stock with a revised TP of INR400, valuing the stock at 7.5x EV/EBITDA on FY28 estimates.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412