Neutral ITC Ltd for the Target Rs 335 by Motilal Oswal Financial Services Ltd

Cigarette price hike in transit; near-term volatility to sustain

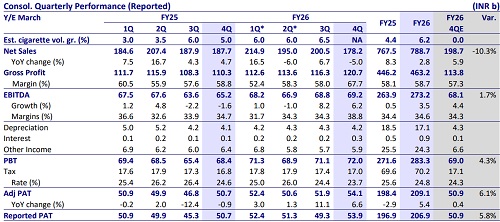

* ITC reported consolidated gross cigarette sales growth of 30% YoY to INR119.5b (est. INR90.4b). Net cigarette sales (INR59.5b) declined 22% given the increase in excise duty. There was a month gap between the new tax announcement date and the implementation date (1st Feb), unprecedented in the history of tax increases. It led to a significant gap between primary and secondary sales, thereby 4Q performance is not comparable. Moreover, given such a sharp increase in taxes, ITC has adopted a calibrated price hike strategy (unlike immediate tax pass-on historically) to protect drop-out of consumers from legal to illegal cigarette markets. Cigarette price hikes are still active, and the cumulative hike has not reached the tax-neutral level.

* Consol. FMCG segment sales grew 15% YoY (beat). A recovery was seen in notebooks despite pressure from low-priced imports and local competition, driven by ITC’s calibrated pricing actions. ITC has seen strong growth across products, with premium offerings continuing to perform well. EBIT grew 52% YoY to INR5.3b (beat) and EBIT margin expanded by 200bp to 8.3%.

* Agri business sales declined 15% YoY to INR31.7b (miss), impacted by geopolitical disruptions and a high base. EBIT margin contracted by 50bp YoY to 6.3% (est. 6%).

* Paper business sales grew 2% YoY to INR22.3b, with a similar muted performance in FY26 (4% growth). The minimum import price (MIP) on virgin multi-layer paperboard led to early signs of improvement in net realizations during the quarter. EBIT grew 19% YoY (on base of 33% decline), while EBIT margin expanded 150bp YoY to 10.4% (miss).

* In cigarette business, the tax hike pass-on to consumers is still in progress. Thus, cigarette revenue and EBIT performance will be quite volatile in the near term (at least up to 1QFY27). Earnings pressure on cigarettes would take away the near-term catalysts (recovery in FMCG and Paper) and valuation comfort. ITC has a full cigarette portfolio to better navigate the tax increase, but competitive pressure from illicit cigarettes will take a toll on the formal cigarette industry. A calibrated price hike is expected to impact cigarette EBIT performance in the near term. We maintain our Neutral rating on ITC with our SoTP-based TP of INR335 (implying 20x FY28E EPS).

Valuation and view

* The price hike on cigarettes is slower than expected and is expected to impact earnings in FY27. This strategy can lower the drop-out of consumers from legal to illegal, but it is adding near-term earnings risk. We cut our EPS estimates by ~3%

* ITC is still under the transitory phase in terms of passing on the entire tax hike to consumers. Thus, we believe the cigarette revenue and EBIT performance will be volatile in the near term (at least up to 1QFY27).

* The FMCG business continues to perform well with robust improvement in margins. However, we believe earnings pressure on cigarettes would take away the near-term catalysts (recovery in FMCG and Paper) and comfort on valuation. ITC has a full cigarette portfolio to better navigate the tax increase, but competitive pressure from illicit cigarettes will take a toll on the formal cigarette industry.

* We maintain our Neutral rating on ITC with our SoTP-based TP of INR335 (implying 20x FY28E EPS)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412