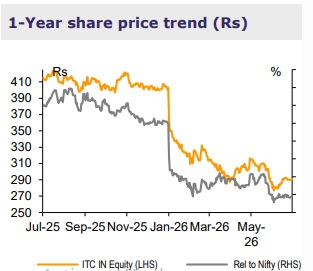

Add ITC Ltd for the Target 310 by Emkay Global Financial Services Ltd

ITC’s FY26 annual report highlights its focus on creating a future-forward enterprise, driven by its ITC NEXT strategy which emphasizes creating new drivers of growth innovation, supply chain agility, digital, etc. The cigarette business is in a flux due to a sharp tax hike, which has hurt volumes. Its FMCGOthers business is now one of the largest FMCG companies in India, with revenue of ~Rs242bn in FY26 (aspires to be the No 1 FMCG firm in India). Balance sheet remains healthy, with strong cash generation of over Rs150bn in FY26. We maintain ADD and TP of Rs310.

Cigarettes – turbulent times ahead due to unprecedented tax hikes

FY26 started well for the company with resilient volume growth, with continued focus on strengthening its product portfolio. In FY26, ITC launched 15+ new products/variants, including Classic Clove, American Club Super Slims, Gold Flake Kings Longs, etc. However, the unprecedented tax hike in Feb-26 disrupted the industry, leading to sharp price increases, mix change, etc, which, in turn, impacted volumes, in our view. We expect the industry to remain in flux over the coming quarters, and expect cigarette volumes to decline by high single-digits. As price increases have largely been lower than the tax hike, we expect EBIT margin to remain under pressure as well

FMCG-Others is on a healthy growth trajectory, with improving margins

ITC’s FMCG-Others segment revenue grew ~10% yoy to Rs242bn, with EBITDA margin expanding by 20bps yoy to 10%. Branded Packaged Foods (84% of sales) drove overall growth, led by market extensions in Aashirvaad, Sunfeast, and Bingo!, alongside macro tailwinds and premiumization. The management fortified its future pipeline by launching ~100 new products, scaling digital acquisitions (Rs13.5bn revenue run rate), and expanding a fresh food cloud-kitchen network.

Other businesses

The Paperboard business navigated early margin pressure from cheap imports and soaring wood costs, recovering in 2HFY26 via cooling raw material prices and import protections (MIP). Agri business was impacted by geopolitical and policy headwinds, and ITC aims to sustain profitability by focusing on high-margin, value-added adjacencies.

Other highlights

1) ITC generated a robust Rs170bn in operating cash flow in FY26 and Rs150bn in free cash flow, maintaining an 85–90% dividend payout ratio.

2) Annual capex rose yoy to ~Rs25bn, led by increases in both cigarettes and FMCG-Others segments.

3) Working capital days increased slightly to 80 days, led by higher inventory days.

4) ITC paid ~Rs4bn to British American Tobacco to acquire assets of three brands (Dunhill, Rothmans, and Benson & Hedges) for the India market.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354