Neutral ACC Ltd for the Target Rs. 552 by Motilal Oswal Financial Services Ltd

.jpg)

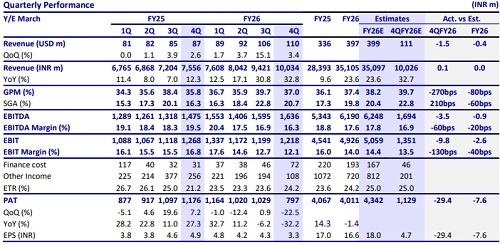

Performance in line; FY27 likely to be better than FY26

* Indegene’s 4QFY26 revenue rose to 6.5% QoQ to INR10b (in line with our estimate), while Ex-BioPharm revenue growth stood at 5.6%. Consequently, EBITDA margin contracted 60bp QoQ to 16.3% (MOFSL estimate: 16.9%), and EBIT margin stands at 12.1%. ? PAT declined by 22.5% QoQ and 32.2% YoY to INR0.8b (MOFSL estimate of INR1.1b), mainly on account of margin dilution and exceptional items.

* In FY26, Indegene’s INR revenue/EBIT/PAT grew 23.6%/8.5%/-1.4% YoY in INR terms. We expect its INR revenue/EBIT/PAT to grow 19.2%/28.1%/32.1% YoY in FY27. We are expecting mid-teens CC revenue growth and gradual margin expansion in FY27. We value the stock at 20x FY28E EPS to arrive at our TP of INR552. We reiterate our Neutral rating on the stock.

Our view:

* Life science and pharma opex outsourcing is a key tailwind. Indegene posted a 18.2% YoY USD growth in FY26; its EBIT margin dipped 200bp YoY to 14.0% due to acquisition-related impact. Management emphasized that enterprise segments will remain the primary growth engine, benefiting from scale, stickiness, and increasing centralization within pharma organizations.

* Management highlighted that from a scalability perspective, today’s USD1m relationship can be a USD25m relationship through a land-and-expand approach. Further, some of these accounts have already scaled to USD5m ACV.

* Margin dipped due to investmentsin GTM, but management believes that as growth momentum revives, profitability and margin will improve from 2HFY27.

* Exceptional items include the provision of INR203m toward the estimated cost of settlement of a lawsuit alleging breach of the Telephone Consumer Protection Act.

* Revenue per employee (RPE) at USD75K was up from USD67K in FY25, led by embedding AI into delivery models, shifting towards outcome-based pricing, and its proprietary Cortex knowledge engineering platform.

* After building foundational capabilities in FY26 through talent investments, GenAI productization, client pilots, and operating model redesign in FY27, the focus will be on scaling revenue.

* In 4Q, it signed one deal of USD3m+ ACV in clinical business with a new client and also closed seven deals of USD1m+ ACV. Within these, four were from Top-20 clients. It expects FY26 deal wins to aid revenue growth in FY27.

Valuation and View:

We raise our earnings estimates considering the impact of new deals and the possibility of increased work outsourcing from the global pharma and life sciences companies amid expanding drug pipelines, rising clinical trial activity, and increasing regulatory complexity for life sciences companies. We expect Indegene to deliver a CAGR of 19%/21%/18% in revenue/EBIT/PAT over FY25-28. We reiterate our Neutral rating with a TP of INR552 (based on 20x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412