Buy ACC Ltd For Target Rs.1,810 By Choice Institutional Equities

Weak FY27 outlook offsets positive

We retain our BUY rating on ACC, while revising our target price downwards to INR 1,810/share (earlier INR 2,200), factoring in 1) Earnings downgrade to ~7.2% for FY27E and ~5.6% for FY28E amid higher input cost, 2) Softer demand growth for FY27E of ~5%, 3) EBITDA/t remains below earlier assumption by ~INR 100/t in FY26 and 4) We cut our EV/CE valuation multiple to 1.6x (from earlier 1.9x). Despite near-term margin headwinds, we remain constructive on ACC long-term outlook, supported by: a) Strategy around strengthening its presence in Southern India market, b) Value-accretive costreduction plan – targeting INR ~250/t cost reduction in FY27E and c) Positive sector tailwinds – we expect healthy pricing environment. We project ACC to deliver an EBITDA CAGR of ~15.8% over FY26– 29E, driven by volume growth of 6.0%/7.0%/8.0% and realisation growth of 1.5%/0.5%/0.5% over FY27E–FY29E, respectively.

Q4FY26: Cost pressure weighs on margin

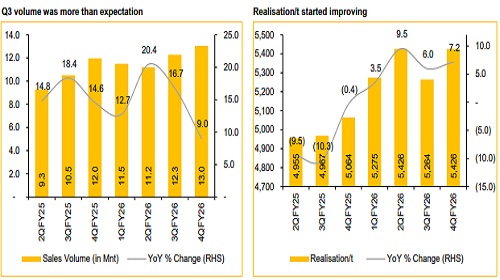

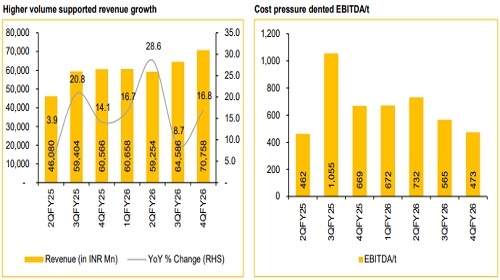

ACC reported Q4FY26 revenue and EBITDA of INR 70,758 Mn (including government grants), (+16.8% YoY, +9.6% QoQ) and INR 6,164 Mn (-23.0% YoY, -11.1% QoQ). Vs CIE est of INR 66,406 Mn and INR 7,380 Mn, respectively. Total volume for Q4 stood at 13.0 Mnt (vs CIE est. 12.4 Mnt), up 9.0% YoY and up 6.3% QoQ.

Blended realisation/t (including RMC volume) came in at INR 5,426/t (+9.5% YoY, +3.1% QoQ), which is higher than CIE est. of INR 5,337/t. Total cost/t came in at INR 4,954/t (+12.7% YoY, +5.4% QoQ). EBITDA/t (including RMC volume) came in at INR 473/t, down 29.4% YoY and 16.4% QoQ.

West Asia headwinds to persist; Cost actions under way:

impacted by elevated cost pressure driven by higher fuel and diesel prices, tight packaging bag availability and INR depreciation — largely linked to the ongoing West Asia crisis. Management expects these headwinds to continue into H1FY27.

We expect cost pressure to remain elevated in Q1FY27, with overall cost inflation likely in the range of INR 120–150/t QoQ, primarily due to fuel and logistics. While mitigation levers should partly offset the impact, near-term margin is likely to remain under pressure before easing from H2FY27.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)