Neutral Anand Rathi Wealth Ltd for the Target Rs.3,100 by Motilal Oswal Financial Services Ltd

In-line performance excluding one-time impacts; FY26 guidance achieved

* Anand Rathi Wealth (ARWM) posted an operating revenue of ~INR2.9b in 4QFY26 (in line), up 30% YoY but flat QoQ, primarily driven by a 35%/24% YoY growth in revenue from the distribution of financial products/MF. For FY26, it grew 22% YoY to INR11.5b.

* Operating expenses for 4QFY26 grew 55% YoY to INR2b, with employee costs/other expenses growing 67%/15% YoY. EBITDA was at INR848m, down 7% YoY, owing to a one-time ESOP impact, with EBITDA margin at 29.5% in 4QFY26 (40.9% in 4QFY25). Excluding the impact, EBITDA was at INR1.2b (in-line), with margins at 43.1% (vs our est. of 44.3%).

* For 4QFY26, consolidated PAT stood at INR1b (+40% YoY). Excluding onetime impacts, PAT came in at INR920m (+25% YoY and in-line) for 4QFY26 and INR3.9b for FY26 (+28% YoY and slightly better than FY26 guidance of INR3.75b).

* Management has guided for FY27 Revenue/PAT/AUM of INR 14.2b/ INR4.6b/INR1.2t, with the long-term growth trajectory remaining intact at 20–25%. MF yields remained stable at ~1.09%. Management indicated that the recent regulatory changes around TER (effective 1st Apr’26) are expected to have minimal impact (~2–4 bp) and are unlikely to materially affect profitability.

* We have broadly maintained our earnings estimates for FY26, FY27, and FY28, as the company remains on track to meet its guidance. We expect AUM/Revenue/PAT to expand at a CAGR of 22%/20%/20%, respectively, over FY26–28, with robust cash generation (INR8.3b of OCF during FY26– 28E), an RoE of over 35%, and a healthy balance sheet. We reiterate our Neutral rating, with a one-year TP of INR 3,100, based on 45x FY28E EPS.

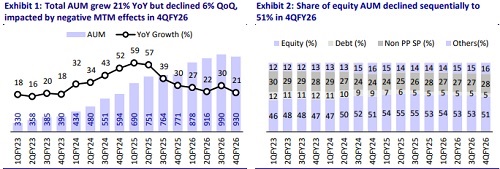

AUM growth impacted by MTM; overall guidance largely met

* Total AUM grew 21% YoY but declined 6% QoQ to INR930b, led by negative MTM impact. The share of equity MFs in the overall AUM mix was 51%, with equity AUM market share stable QoQ at 1.46% in Mar’26. Private Wealth/Digital Wealth AUM grew 21%/22% YoY to INR908b/INR22b.

* Total quarterly net inflows/equity flows declined 3%/flat YoY to INR33.8b/INR18.9b. On an annual basis, total/equity flows grew modestly at 7%/3% YoY, impacted by volatile markets. Equity inflows as a proportion of total stood at 56% vs. 54% in 4QFY25. ? Monthly SIP flows for Mar’26 increased 32% YoY to INR920m.

* The share of customers with AUM of over INR500m increased to 28.9% in 4QFY26 from 24.6% in 4QFY25. The company onboarded 133 net new client families in 4Q, taking the total count to 13.4k families. Operating expenses for 4QFY26 grew 55% YoY to INR2b, with employee costs growing 67% YoY to INR1.7b, owing to ESOP expenses of INR393m. Other expenses grew 15% YoY to INR345m. Excluding the one-time ESOP impact, opex was in line with our estimates.

* Other income for the quarter came in at INR684m, rising 252% YoY, driven by an INR546m worth of fair value gain on an investment in Anand Rathi Global Finance Limited. This resulted in a PBT of INR1.4b (+41% YoY). Excluding the one-time ESOP and other income impact, PBT was INR1.25b (+26% YoY), in line with our estimates.

* The company reported one of the lowest client attrition rates in the industry, with only 0.23% of AUM lost in 4QFY26. RM attrition remained minimal, with one exit during the quarter holding AUM of greater than INR400m. About 75% of the AUM associated with the RM attrition has been retained.

* AUM per RM increased to INR2.3b in Mar’26 from INR2b in Mar’25, driven by the continued association of RMs with the organization. Additionally, clients per RM improved to 33 from 31 in 4QFY25.

Highlights from the management commentary

* MF yields remained stable at ~1.09%. Management indicated that recent regulatory changes around TER (implementing from 1st Apr’26) are likely to have minimal impact (2–4 bp range) and are not expected to materially affect profitability.

* Management has guided for revenue of INR14.2b and PAT of INR4.6b, along with an AUM target of INR1.2t for FY27. The long-term growth trajectory of 20– 25% remains intact.

* The company recorded a non-recurring ESOP expense of INR393m during the quarter, arising from the accounting treatment of stock option grants. Additionally, it recognized a fair value gain of INR546m on its investment in Anand Rathi Global Finance Limited, which is MTM in nature and not driven by any stake sale.

Valuation and view

* ARWM is one of the few companies in the listed space that has consistently met its stated guidance. For FY27, management has guided for revenue/PAT of INR14.2b/INR4.6b vs. our estimates of INR13.7b/INR4.6b.

* We have broadly maintained our earnings estimates for FY26, FY27, and FY28, as the company remains on track to meet its guidance. We expect AUM/revenue/PAT to expand at a CAGR of 22%/20%/20%, respectively, over FY26–28. This growth is supported by robust cash generation (INR8.3b of OCF during FY26-28E), an RoE of over 35%, and a healthy balance sheet. We reiterate our Neutral rating, with a one-year TP of INR 3,100, based on 45x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041