Buy Fusion Finance Ltd for the Target Rs 235 by Motilal Oswal Financial Services Ltd

Broad-based improvement in CE; earnings to accelerate from 2H FY27 AUM target of ~INR100b intact

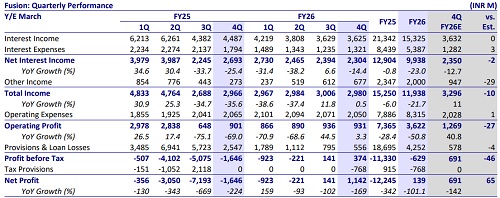

* Fusion Finance (FUSION) reported a net profit of ~INR1.1b in 4QFY26 (vs. est. of INR691m). Fusion recognized a DTA of INR768m in 4QFY26 – this led to tax write-backs in the quarter. FY26 PAT stood at ~INR139m (vs. a loss of ~INR12.2b in FY25). NII in 4QFY26 declined ~14% YoY to ~INR2.3b (in line). Opex was flat YoY at INR2.05b (in line). The cost-to-income ratio remained stable QoQ at ~69% (PQ: ~69% and PY: ~70%).

* PPoP rose ~3% YoY to ~INR931m (27% miss). FY26 PPoP declined ~51% YoY to ~INR3.6b. Net credit costs declined sequentially to ~INR556m (inline). Annualized credit costs in 4QFY26 declined ~150bp QoQ to ~3.6% (PQ: ~5.1%).

* Fusion has targeted an AUM of ~INR 100b by FY27, supported by a disciplined customer acquisition strategy and a continued focus on lowleveraged, stable borrower profiles. MSME is expected to be a key growth driver, led by deeper market penetration, increasing focus on the LAP segment, and expansion through new sourcing channels to strengthen origination and reach.

* The company’s branch segmentation strategy, which classifies branches into A to D categories based on operating metrics and growth behavior, is enabling further calibrated expansion and better risk alignment at the branch level. Additionally, the ongoing platform migration is expected to materially enhance onboarding, servicing, and branch efficiency, thereby strengthening operational scalability and supporting sustainable, high-quality growth.

* NII in 4QFY26 remained subdued, primarily due to a broadly flat average AUM base along with higher liquidity buffers and lower DA income, which together temporarily weighed on income recognition. Going forward, NII is expected to grow in 1QFY27 and further accelerate from 2QFY27, thereby supporting PPoP growth. Asset quality remains strong and well-controlled, supported by robust CE of ~99.7%-99.8% across key markets, with GNPA/NNPA at ~3.2%/~0.5%, reflecting contained stress levels. Recoveries from written-off accounts remain healthy, with 90+ DPD recoveries exceeding ~INR350m, underscoring disciplined underwriting and tight portfolio monitoring.

* Fusion has demonstrated steady improvement across key operating parameters, reflecting stronger execution discipline and a refined risk framework. With a clear strategic direction and continued focus on qualityled growth, it is well positioned to scale its guided AUM to INR100b by FY27, implying ~35% growth over the base. This expansion is expected to be supported by improving asset quality trends and a strengthening MSME franchise. Backed by tighter customer selection and operational enhancements, the company is building a more resilient and sustainable growth model going forward.

* With recovery gaining traction, we expect Fusion to deliver an AUM CAGR of ~25% over FY26E-28E with a RoA/RoE of ~3.8%/ 13% by FY28E. We reiterate our BUY rating with a revised TP of INR235 (based on 1.2x FY28E P/BV)

Strong asset quality with improving CE and lower delinquencies

* GS3 declined ~120bp QoQ to ~3.2%, while NS3 declined ~12bp QoQ to 0.5%. Stage 3 PCR stood at 85% (PQ: 86.3%). Stage 2 dipped ~70bp QoQ to 1.0% and S2 PCR improved ~5pp QoQ to ~71.4%.

* The company has a management overlay of INR195m remaining after the release of INR100m in 4QFY26.

* Avg. CE (MFI) improved to 99.66% in 4Q (vs. 99.14% in 3Q). New book (MFI) is now at 87% of the portfolio with Avg. CE at 99.77% in 4Q. Net forward flow rate was < 0.1% in 4QFY26. Fusion’s + >=3 borrowers declined to ~5% (PQ: 6.8%).

* We expect Fusion’s credit costs to decline sharply from ~6% in FY26 to ~3.2%/ 3.1% in FY27E/FY28E.

Highlights from the management commentary

* Fusion expects FY27 opex to increase by ~5-6% over FY26 levels despite business growth, supported by branch rationalization and operating efficiency initiatives. Management is also taking external expert support to further improve branch productivity and cost efficiency.

* Fusion had not recognized DTA over the past 4-5 quarters and has now resumed DTA recognition. Total DTA stood at ~INR3.9b, of which ~INR3.1b remains available for future utilization over the next 12-18 months.

Valuation and view

* Fusion reported a decent earnings performance in 4QFY26, supported by DTA recognition, tax write-backs, and further moderation in credit costs. Disbursement momentum continued to improve, with steady scale-up in the MFI book underpinned by prudent underwriting, as reflected in stronger collection efficiency and easing forward flow trends. Asset quality also remained resilient with continued improvement in key operating metrics, reinforcing the overall stability of the portfolio.

* Fusion currently trades at 1.1x FY27E P/B. With recovery gaining traction, we expect Fusion to deliver an AUM CAGR of ~25% over FY26E-28E with a RoA/RoE of ~3.8%/ 13% by FY28E. We reiterate our BUY rating with a revised TP of INR235 (based on 1.2x FY28E P/BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412