Buy Privi Speciality Chemicals Ltd for the Target Rs 3,900 by Motilal Oswal Financial Services Ltd

Resilient operations, strategic expansion, and biomass integration drive a strong growth outlook

* The Middle East crisis since Mar’26 has disrupted energy supply chains and raised specialty chemical prices due to the sector’s reliance on crude-linked feedstocks. Despite the industry’s high oil dependency (~58%), PRIVI remains relatively insulated, with only ~25% exposure, limited reliance on the Strait of Hormuz, and negligible dependence on Middle Eastern markets. This supports greater operational stability and margin resilience.

* PRIVI’s merger with Privi Fine Science (PFS)/Privi Biotechnologies (PBPL) (by 3QFY27) is expected to add ~5–7% to FY27 revenue and expand its specialty aroma portfolio. Further, PRIGIV (the JV with Givaudan) has turned PAT-positive, with profitability expected to further improve, supported by fresh funding and debt reduction. Further capex into high-value molecules and tech-led expansion should drive steady growth and margin gains.

* PRIVI is expanding into high-value specialty products such as Maltol, Ethyl Maltol, and Cyclopentanone, which could contribute over INR5b in revenues by FY28, while supporting strong margins and cost efficiencies. The company’s planned backward integration into Furfural is expected to materially improve profitability, aided by the stable availability of low-cost corn cobs as feedstock.

* PRIVI’s ‘Beyond 5K:1K’ (INR50b/INR10b of revenue/EBITDA by FY30) strategy is centered on building a biomass-based biorefinery platform, targeting ~USD5b (total TAM to reach ~USD11.1b) opportunity across high-value specialty chemicals such as vanillin, lactic acid, and xylitol. Unlike conventional biofuel models, the company is focusing on premium molecules with superior economics and scalable demand potential. The upcoming demonstration plant will be critical in validating commercial viability, while successful execution could position PRIVI as a sustainable, lower-cost alternative to conventional fossil-fuel-based chemical manufacturing.

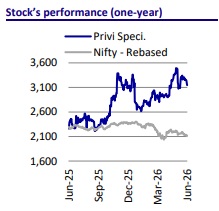

* We expect PRIVI to clock a CAGR of 25%/27%/34% in revenue/EBITDA/PAT during FY26-28. We reiterate our BUY rating with a TP of INR3900 (based on 27x FY28E EPS i.e. 3 year average – one year forward P/E).

Integrated biomass strategy to support growth and margin expansion

* The company is expanding its product line to include Maltol, Ethyl Maltol, and Cyclopentanone, targeting its current flavor and fragrance customer base. These initiatives could drive ~INR5b+ revenues, strong margins, and improved cost efficiencies in FY28.

* The company plans to invest in backward integration for Furfural as a raw material, which is expected to expand margins by 50% (requires corn cob as a key raw material, manufacturing process in Exhibit 1).

* India’s maize production has been witnessing a steady uptrend, supported by policy incentives and strong end-use demand. According to the Ministry of Agriculture & Farmers Welfare, output has risen from ~32 MMT in FY21 to ~42 MMT in FY25 (8% CAGR over the period), driven by MSP support and expansion in rabi cultivation.

* This creates a favorable structural environment for PRIVI, as higher maize output increases the availability of corn cobs—an agricultural residue used as feedstock in its biomass-based chemical chain. Unlike maize grain, cobs have limited competing demand, resulting in relatively stable and low input costs.

* PRIVI’s specialty chemical expansion and Furfural backward integration are expected to drive strong revenue growth and margin expansion over the medium term. Rising maize output in India also supports stable availability of low-cost corn cobs, strengthening the company’s cost competitiveness and supply security.

Valuation and view

* PRIVI is well-positioned for sustainable growth, supported by its relatively low crude-linked exposure (~25%), which provides resilience against ongoing energy market volatility and supports margin stability. The upcoming mergers with PFS/PBPL and PRIGIV JV are expected to expand its specialty aroma portfolio. Consequently, this is expected to drive revenue growth and enhance earnings.

* Further, the company’s expansion into high-value specialty molecules such as Maltol, Ethyl Maltol, and Cyclopentanone (from the Corn Cob route), coupled with backward integration into Furfural, is expected to contribute meaningfully to revenues while improving cost competitiveness and margins.

* We expect PRIVI to clock a CAGR of 25%/27%/34% in revenue/EBITDA/PAT during FY26-28. We reiterate our BUY rating with a TP of INR3900 (based on 27x FY28E EPS i.e. 3 year average – one year forward P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412