Debt Outlook : A Liquidity-Led Bond Market as the RBI Extends Its Pause by Sneha Pandey, Fund Manager- Fixed Income, Quantum AMC

The Indian fixed income market enters the second half of FY27 with a macro backdrop that is becoming increasingly supportive for bonds, even as inflation risks remain on the horizon.

While geopolitical uncertainties and commodity price volatility continue to dominate global markets, domestic financial conditions have eased materially following the Reserve Bank of India's liquidity and foreign exchange measures announced in its June 26 monetary policy.

The debate, therefore, is gradually shifting from "whether liquidity will improve" to "how the RBI will eventually manage the surplus."

Our base case is that the RBI is likely to maintain an extended pause in the policy repo rate through December 2026. Although inflation is expected to edge higher over the coming quarters owing to cost pass-through and weather-related food price risks, monetary conditions remain sufficiently accommodative to allow the central bank to wait for greater clarity before contemplating any policy tightening.

More importantly, liquidity has emerged as the dominant driver for domestic fixed income markets. The RBI's comprehensive foreign exchange package - comprising concessional swap facilities for FCNR(B) deposits, incentives for external commercial borrowings (ECBs), regulatory relaxations and measures aimed at attracting durable foreign currency inflows - is expected to materially improve liquidity while supporting external sector stability.

These measures should help offset global capital flow volatility, strengthen the balance of payments and provide an important anchor for the rupee.

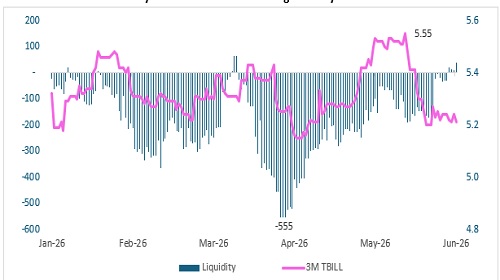

With liquidity expected to remain comfortably in surplus, overnight and short-term money market rates have already eased significantly and are likely to remain near or even below the policy corridor for some time. Treasury bill yields, overnight funding rates and short-duration instruments should continue to benefit as liquidity suppresses funding costs across the banking system.

Chart I: Money market rates have eased significantly in June 2026

However, a prolonged liquidity surplus is unlikely to be left completely unchecked. As foreign currency inflows gather pace and banking system liquidity expands further, the RBI could increasingly rely on liquidity absorption measures rather than policy rate action.

Open Market Operation (OMO) sales therefore become a distinct possibility during the second half of the year to sterilize excess liquidity without altering the monetary policy stance. Should surplus liquidity become more persistent, a calibrated increase in the Cash Reserve Ratio (CRR) cannot be ruled out as an alternative liquidity management tool. Such measures would represent liquidity normalization rather than monetary tightening.

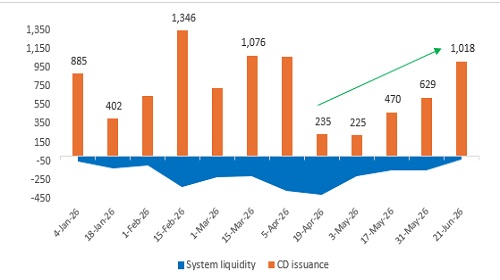

Robust credit growth of around 18% continues to outpace deposit mobilization, keeping the banking system's credit-to-deposit ratio elevated above 82%. This structural funding gap has become increasingly visible in recent months, reflected in the sharp pickup in certificate of deposit (CD) issuances during June 2026 as banks tapped wholesale funding markets to bridge incremental funding requirements. Elevated CD issuance highlights that while system liquidity is abundant, funding remains unevenly distributed across institutions, particularly for banks experiencing faster loan growth than deposit accretion.

Chart II: CD issuances pick up pace as deposit mobilization continues to lag credit growth

Nevertheless, the RBI's recent foreign currency measures could gradually ease these funding pressures. FCNR(B) inflows, ECB mobilization and overseas borrowings provide banks with an additional funding avenue, reducing reliance on domestic deposits while simultaneously improving rupee liquidity through the RBI's swap mechanism. This could alleviate upward pressure on wholesale funding costs over time while enhancing overall banking system liquidity.

The fiscal outlook, while facing some near-term pressures, is unlikely to pose a significant challenge for the bond market. Higher expenditure arising from energy-related support measures may lead to a modest fiscal slippage relative to the Budget estimates. However, the impact on market borrowing is expected to remain contained, supported by alternative funding sources, disinvestment proceeds and other fiscal offsets. Consequently, we do not expect any material upward revision in the government's borrowing programme.

From a currency perspective, the outlook has improved meaningfully. Lower crude oil prices together with anticipated FCNR(B) deposits and ECB inflows are expected to strengthen India's balance of payments position, limiting downside risks to the rupee despite an uncertain global environment. While these inflows are largely temporary and repayable in nature, they should provide an effective bridge over the near term and reduce pressure on foreign exchange reserves. Sustained currency stability would, in turn, reduce imported inflation risks and reinforce confidence in domestic fixed income markets.

Against this backdrop, the domestic bond market appears well positioned. The RBI's likely policy pause, abundant liquidity, moderating money market rates and improved external sector dynamics provide a constructive environment for duration.

While inflation risks warrant vigilance and may eventually require calibrated liquidity normalization through OMO sales or CRR adjustments, these measures are unlikely to derail the broader fixed income outlook. Instead, they would represent the RBI's effort to balance financial stability with abundant liquidity rather than the beginning of an aggressive tightening cycle.

In this evolving environment, flexibility is likely to be more valuable than a static investment approach. Dynamic Term funds, with the ability to actively adjust portfolio duration in response to changing interest rate and liquidity conditions, may be better positioned to capture opportunities across the yield curve than fixed maturity strategies, which remain locked into a predetermined duration profile.

At the same time, investors should avoid layering multiple sources of risk within their debt portfolios. With interest rate cycles expected to remain fluid, adding lower credit quality in pursuit of incremental yields may not offer an attractive risk-reward trade-off. A prudent strategy would be to actively manage duration while maintaining a high-quality portfolio comprising predominantly G-Secs and AAA-rated PSU securities. This allows investors to participate in potential duration gains while keeping credit risk to a minimum, resulting in a more resilient fixed income portfolio amid an evolving macroeconomic landscape.

Tag News

Resistance : 24150 (Pivot Level) and 24300 (Key Resistance) by GEPL Capital Ltd