Buy Jain Resource Recycling Ltd for the Target Rs. 560 by Motilal Oswal Financial Services Ltd

Copper price volatility and West Asia crisis impact margins

Operating performance misses estimates

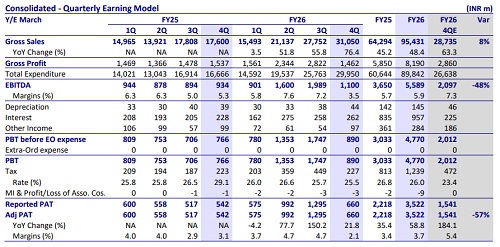

* Jain Resource Recycling (JAINREC) reported EBITDA growth of 18% YoY despite constrained scrap availability, volatile copper prices, and elevated logistics costs. Revenue grew 76% YoY to INR31.7b (blended volume/realization up 12%/57%), led by YoY growth in the copper and lead businesses of 2.5x and 26%, respectively.

* We believe the sharp margin contraction in 4QFY26 is temporary in nature, as it was primarily driven by exceptional copper volatility following the sharp spike in LME prices, along with geopolitical supply chain disruptions. With copper realization formulas transitioning toward longerterm ‘green formula’ contracts, which are showing signs of normalization in 1QFY27 negotiations, along with supplies increasingly being rerouted through alternative shipping routes, material availability is improving. Consequently, we expect a gradual recovery in profitability of the copper segment going forward.

* Factoring in lower-than-estimated earnings in 4Q, we reduce our FY27/FY28 earnings estimate by 15%/16% and reiterate our BUY rating on the stock with a TP of INR560 (premised on 27x FY28E EPS).

Healthy volume growth; EBITDA impacted by exceptional volatility

* Consolidated revenue grew 76% YoY to INR31.1b (est. INR28.7b) in 4QFY26.

* EBITDA rose 18% YoY to INR1.1b (est. INR2.1b). EBITDA margins contracted ~180bp YoY to 3.5% (est. 7.3%) due to gross margin contraction of 400bp YoY to 5%. The EBITDA impact of ~INR6,000/MT was due to shipping, fuel, and energy cost inflation, while ~INR18,000- 18,500/MT impact was from the change in formula and copper volatility.

* Adj. PAT grew 22% YoY to INR660m (est. INR1.5b).

* Lead business revenue grew 26% YoY to INR10.5b, led by a 19% YoY realization growth. Volume stood at 45KMT in 4QFY26 (up 2% YoY). EBITDA/MT stood at INR17,614 (up 19% YoY) for the quarter.

* Copper business revenue grew 2.5x YoY to INR19.4b. Volumes stood at 16.8KMT, up 88% YoY, while EBITDA/MT declined 17% YoY to INR14,160.

* The aluminum business dipped 17% YoY to INR1.1b due to a YoY decline of 34% in volumes to 3.4KMT. EBITDA/MT grew 39% YoY to INR33,432.

* For FY26, revenue/Adj. EBITDA/Adj. PAT grew 48%/53%/59% to INR95b/INR5.6b/INR3.5b.

* CFO for the year stood at negative INR60b vs INR36m in FY25. Net debt stood at INR9b for the year vs INR6.4b in FY25.

Highlights from the management commentary

* Guidance: Management expects lead volumes to grow ~10-15%, while copper volumes are likely to grow 15%+ going forward. Copper utilization is expected to improve materially over the next 2-3 years, with lead operations remaining near peak utilization. Working capital days are targeted to reduce to below 60 days vs 66 days in FY26. Operating cash flow is expected to turn positive from 2QFY27 onward.

* Forward integration: Copper downstream expansion remains the company’s key strategic focus. Copper anode production commenced in Mar’26 with 800 MT/month capacity, while another 800 MT/month furnace is expected in 1QFY27. Copper cathode Phase-1/2 commissioning is targeted in 2QFY27/3QFY27, taking the total capacity to 1,500 MT/month. Copper wire rod and busbar/profile projects are expected to be commissioned by Aug’26 and Sep’26, respectively. Management expects downstream copper products to improve EBITDA/kg by an additional INR20-45, while also enhancing product mix, customer stickiness, and earnings stability.

* Copper business: 4QFY26 margin pressure was driven by a sharp copper price volatility and geopolitical logistics disruptions. Copper prices rose ~40%, leading to a formula contraction after strong 3QFY26 tailwinds from Chinese demand. Management indicated that this formula-led margin contraction is temporary, and its shift toward longer-term ‘green formula’ contracts is likely to negate this phenomenon in the future. The copper business remains fully hedged, with normalized EBITDA expected at ~INR32,000-34,000/ton vs elevated ~INR42,000/ton in 3QFY26.

Valuation and view

* As a leading player in India’s rapidly growing recycling industry, JAINREC is on a growth trajectory, aided by rising demand for recycled/green metals and a regulatory shift favoring organized players, along with the growth of demand for lead and copper in India outpacing the global demand growth.

* Further, to move up the value chain and capitalize on the strong long-term demand outlook for copper, driven by renewable energy, data centers, and EVs, JAINREC is focusing on higher-value copper products, which are expected to expand margins and improve earnings visibility.

* We expect a CAGR of 27%/31%/42% in revenue/EBITDA/PAT over FY26-28. We value the stock at 27x FY28 EPS to arrive at our TP of INR560 and reiterate our BUY rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041