Buy ICICI Lombard Ltd for the Target Rs 2,240 by Motilal Oswal Financial Services Ltd

Building tech moat for scale

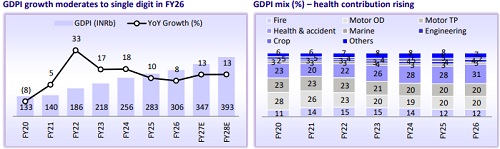

* ICICI Lombard (ICICIGI) is undergoing an important transition after a 25-year journey of redefining India’s insurance sector. Over the last 25 years, the insurer has served 500m customers while building digital infrastructure, strengthening distribution capabilities and enhancing customer engagement. FY26 reflects a shift toward monetizing these investments through enterprisewide execution.

* The company’s outperformance in retail health (+51% YoY vs. +20% YoY for industry) has been a function of (

1) strengthening distribution – 25,000 agents added in FY26

(2) continued innovation – ‘Elevate’ enhanced with new features/persona-based products launched

(3) tech enhancement – deployment of recommendation engine to select appropriate sum insured

(4) customer engagement – scaling up IL Sahayak to 60 cities and 3,000 hospitals for on-ground assistance and superior customer experience.

* Motor segment remains a cornerstone of the franchise, protecting 250m+ drivers since inception. FY26 witnessed a slow start due to low vehicle sales, which improved after GST rationalization in 2HFY26 (15% YoY growth in 4QFY26 vs. 10% for industry). The key areas driving market share dominance (10.7% in FY26) –

(1) granular portfolio segmentation

(2) innovative services like fleet management, IL Smart assist, etc

(3) real-time motor claim tracking ensuring customer satisfaction.

* ICICIGI’s distribution engine has been strengthened further with transition to a multi-line business model from a single-product business model to drive cross-selling, higher customer lifetime value, strong retention and agent productivity. The insurer has additionally invested in capability building initiative (Shiksha Abhiyan), on-ground partner engagement (Unified Branch Meets) and high-impact agency engagement (Bandhan) to empower partners and improve productivity.

* In FY26, ICICIGI introduced a broader vision of intelligent transformation powered by artificial intelligence (AI), building on an existing strong data foundation. AI is increasingly being embedded across underwriting, claims, servicing, customer engagement and operational decision-making across lines of businesses. Apart from enhanced visibility and stronger execution oversight with respect to the organization, tech investments have helped to enhance customer journeys.

* Valuation: Backed by a solid 25-year experience along with continued value addition across business lines, ICICIGI appears well positioned to harness the profitable growth opportunities in the under-penetrated general insurance sector. Leadership in Motor insurance, accelerating momentum in Retail Health, expanding distribution capabilities, growing AI integration and a strong balance sheet remain the key growth drivers. We expect ICICIGI’s GWP/PAT to expand at a CAGR of 12%/19% over FY26-28 as CoR declines to 101.7% by FY28. Reiterate a BUY rating on the stock with a TP of INR2,240 (based on 28x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)