Neutral Divi’s Laboratories Ltd for the Target Rs. 6,765 by Motilal Oswal Financial Services Ltd

Record revenue; CS on a 10-quarter winning streak

Superior execution underpins 18% earnings CAGR; premium multiple caps upside

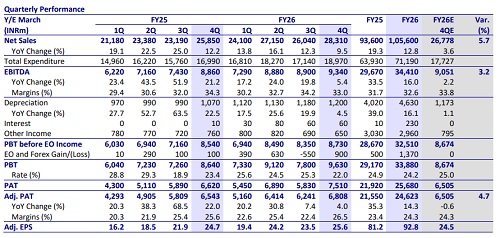

* Divi’s Lab (DIVI) delivered a better-than-expected financial performance in 4QFY26, with a 6%, 3%, 5% beat on revenue, EBITDA, and PAT, respectively. DIVI recorded the highest-ever quarterly revenue in 4Q.

* The CS segment has seen steady sales in 4Q and has posted 10 quarters of robust YoY growth. Notably, FY26 is the second straight year of strong YoY growth, led by the scale-up of existing contracts and the addition of new contracts.

* While pricing pressure continues to persist in the API segment, DIVI has been driving business through higher volume throughput and gaining market share. It has also worked with its customers to introduce newer molecules in this segment, subject to regulatory approvals.

* DIVI delivered high-teens YoY growth in the nutraceuticals segment as well through capacity expansion and strengthening its position in this segment.

* We trim our earnings estimate for FY27/FY28, factoring in 1) increased opex related to logistics due to the geopolitical turmoil, and 2) a gradual off-take of certain contracts such as contrast media products. We value DIVI at 52x 12M forward earnings to arrive at our TP of INR6,765.

* DIVI remains focused on execution discipline, supply reliability, and longterm capacity addition. It is also deepening capabilities in continuous flow chemistry, biocatalysis, peptides, contrast media space, etc., to provide superior and consistent service to innovator customers. DIVI continues to work on cost efficiency in manufacturing API in the generics segment, driving better volume share, as well as expanding the product offerings. We model an 18% earnings CAGR over FY26-28.

* Considering 63x/53x FY27/FY28E P/E, the current valuation adequately factors in the earnings upside. Reiterate Neutral.

Input cost inflation and pricing pressure drag margins

* DIVI’s revenue grew 9.5% YoY to INR28.3b (our est: INR26.8b) for 4QFY26.

Gross margin contracted 160bp YoY to 60.5%.

* EBITDA margin contracted 130bp YoY to 33% (our est: 33.8%), mainly due to a contraction in gross margin.

* EBITDA grew 5.4% YoY to INR9.3b (our est: INR9.0b) for 4QFY26.

* Adjusted for INR900m in forex gains, PAT grew 4% YoY to INR6.8b (our est: INR6.5b).

* For FY26, DIVI’s revenue/EBITDA/PAT grew 13%/16%/14% YoY.

Highlights from the management commentary

* DIVI intends to grow revenue in double digits on a YoY basis in FY27.

* While inventory increase has been moderate in 4QFY26 on a QoQ basis, there has been a reasonable increase in the inventory in 1QFY27, considering the external geopolitical issues.

* Most of the current API segment revenue growth was driven by better volume offtake of existing products. DIVI is working with customers for new product launches. This would support growth going forward.

* DIVI has commercialized iodine-based products. The gadolinium contrast media products are at the qualification stage. DIVI continues to support customers for regulatory approval.

* CWIP was INR21b at the end of FY26. DIVI has capitalized assets worth INR15.4b, of which INR8b was capitalized in 4QFY26.

* DIVI is steadily increasing the production level at Unit 3 and shifting the production from Unit 1/2 to meet the customer’s requirements.

* The Nutraceutical business was INR9.4b/INR2.4b for FY26/4QFY26.

* DIVI has several 3,000L-capacity reactors for manufacturing peptides. DIVI aspires to be the leading manufacturing capacity for peptides at the global level.

* It has several customers in the peptides space at various stages of development.

* Exports stood at 89% of the sales. The US/EU formed 74% of the export sales for FY26.

* Receivable/Inventory at the end of FY26 was INR30b/INR39.5b.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412