Neutral Aegis Logistics Ltd for the Target Rs 706 by Motilal Oswal Financial Services Ltd

Strong 4QFY26 performance

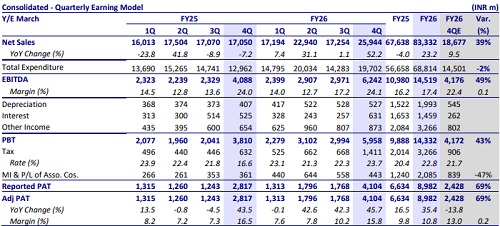

* In 4QFY26, revenue for Aegis Logistics (AEGISLOG) came in 39% above our expectations at INR25.9b, while EBITDA came in 49% above our estimate at INR6.2b. EBITDA margin stood at 22.4% (4QFY25 margins: 24%). The Liquids division’s revenue was INR1.8b (-24% YoY), and EBIT was INR1b (-43% YoY). The Gas division’s revenue stood at INR24.1b (+65% YoY), and EBIT was INR5b (+131% YoY). PAT came in 69% above our estimate at INR4.1b.

* Key things we liked about the result:

1) Gas distribution EBITDA/mt increased to ~INR7,000 (vs. historical levels of ~INR4,000). Further, management believes margins can remain around current levels even under a normalized energy price environment as volumes continue to scale.

2) The Kandla-Gorakhpur pipeline connectivity to Kandla and Pipavav terminal is expected in 2QFY27, boosting evacuation at both terminals.

3) Management reiterated its aspiration of reaching ~2mt of LPG/ammonia distribution volumes by FY28.

4) Management outlined a cumulative investment opportunity of ~USD5b by FY31. Around USD1.2b of investments are expected by Mar’27, followed by another ~INR50b by Mar’28.

5) The company is evaluating a 60k cbm liquid terminal at Kochi and Mangalore port, each, providing incremental growth optionality beyond the currently announced project pipeline.

* Key monitorables:

1) Government initiatives promoting PNG adoption and reducing LPG dependence could potentially moderate long-term LPG demand growth.

2) Industry LPG imports from the Middle East reportedly declined 30%- 50% during Apr-May’26, driven by geopolitical disruptions. However, management expects normalization from 2QFY27 onward as sourcing diversifies.

3) With a substantial portion of the USD5b investment pipeline likely to be deployed during FY29-31, project execution, funding mix, and leverage trajectory remain key monitorables.

* Valuation : We reiterate our Neutral rating on the stock with a TP of INR706, as we now value the company at 25x Dec’27E EPS of INR28.3.

Valuation and view: Reiterate Neutral

* AEGISLOG has reiterated its ambitious capex plan for:

1) The commissioning of 64,000 kl liquid capacity at the Mumbai port in 1HFY27 (INR1.25b)

2) additional liquid, LPG, and LPG bottling capacity at JNPA (INR16.8b)

3) 94k cbm liquids capacity at Kandla in FY27

4) ammonia terminals at Kandla

5) 36,000 mt of ammonia capacity at Pipavav by 1HFY27.

* While we estimate a 9% CAGR in PAT over FY26-28, we believe that the current valuations at 36x FY27E EPS already factor in the strong expansion in capacity and earnings. We value the stock at 25x Dec’27E EPS of INR28.3 to arrive at our TP of INR706. We reiterate our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412