Buy Lupin Ltd For the Target Rs.2500 By the Axis Securites

Recommendation Rationale

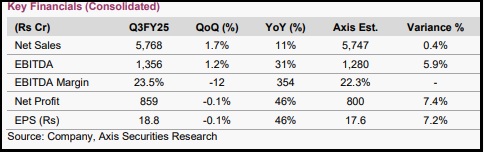

A strong set of results: Lupin reported a strong set of results that exceeded our expectations. Reported revenue grew by 11% YoY, led by the India and US businesses, which grew by 11.9% and 12.3%, respectively, YoY, and the EMEA business, which grew by 20.9% YoY. However, the Emerging Markets business declined by 4.7% YoY, and API shows a gradual recovery with 4% YoY growth.

Improvement in gross margin: The company’s gross margin improved by 330 bps YoY and remained flat QoQ, driven by a favourable product mix, lower input costs, a reduced share of in-licensed products, and increased cost efficiencies.

EBITDA margins improved by 350bps YoY and remained flat QoQ. Reported PAT grew by 40.1% YoY, surpassing expectations.

Sector Outlook: Positive

Company Outlook & Guidance: Lupin has a strong pipeline of niche products that could support double-digit growth in the U.S. market. Injectable products like Glucagon and Dalbavancin, with a market opportunity of $500 Mn, are expected to launch within six months. Additionally, Liraglutide and Risperidone could contribute to revenue in FY27E. Lupin is exploring opportunities in biosimilars, including Ranibizumab and Aflibercept, with Tolvaptan expected to add revenue in the generic segment.

Current Valuation: PE32x for Q1FY27 earnings

Current TP: Rs 2,500/share (Earlier TP: Rs 2,600/share)

Recommendation: BUY

Financial Performance Lupin reported a strong set of results that exceeded our expectations. Reported revenue grew by 11% YoY, led by the India business as well as the US business, which grew by 11.9%/12.3% respectively YoY, and the EMEA business, which grew by 20.9% YoY. However, the Emerging Markets business declined by 4.7% YoY, and API showed a gradual recovery with 4% YoY growth. Gross margins improved by 330 bps YoY and remained flat QoQ, driven by a favourable product mix, lower input costs, a reduced share of in-licensed products, and increased cost efficiencies. EBITDA margins improved by 350 bps YoY and remained flat QoQ. Reported PAT grew by 40.1% YoY, surpassing expectations. Lupin reported U.S. sales of $235 Mn, reflecting a 10.8% YoY growth in constant currency and an overall reported revenue of Rs 2,121 Cr, up 12.3% YoY. This growth was primarily driven by volume expansion in inline products and new product contributions, though pricing pressure and competition in Suprep and Albuterol affected performance.

Financial Performance (Cont’d)

India Business: Lupin reported Rs 1,931 Cr in Q3FY25, registering robust 11.9% YoY growth, driven by strong performance in chronic therapies such as diabetes, cardiology, and gastroenterology, which outpaced market growth. The company strengthened its portfolio by acquiring Eli Lilly’s human insulin range and three trademarks from Boehringer Ingelheim. While the India formulations business grew 9.1% for the nine months, muted growth in the respiratory segment impacted overall performance. Lupin remains confident in maintaining above-market growth, backed by new product launches, in-licensed products, and an extensive 10,000-member sales force.

Valuation & Recommendation Lupin's strong pipeline in generics, biosimilars, and specialty drugs could drive double-digit growth in the U.S. market. Additionally, the company is continuously gaining market share in the diabetes and cardiac segments in India, supported by a 10,000-strong medical representative team that is outpacing industry growth. We recommend a BUY rating with a target price of Rs 2,500/share.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633