Buy KEI Industries Ltd For Target Rs. 4,550 By JM Financial Services

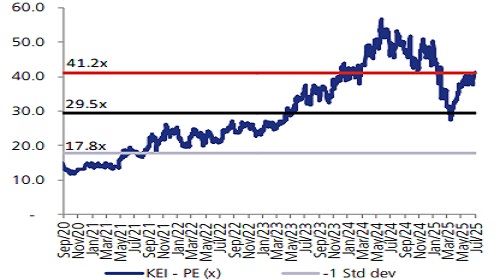

KEI’s 1Q numbers were a beat on JM and street estimates. 1Q revenue at INR 26bn, rose 26% YoY and PAT at INR 2bn, rose 30% YoY. KEI’s strong 1Q performance was driven by robust growth in, both, the domestic and export segments. Within the domestic business, both institutional (+39% YoY) and retail (+22% YoY) channels grew well. Further, KEI’s export business registered a 121% YoY growth. Incrementally, in line with the company’s strategy, revenue from the EPC segment declined. Management has guided for 18% revenue growth for FY26 (likely to beat) and 20% CAGR over the coming 2-3 years. We raise our FY26-28E EPS estimates by 0-4%, and maintain BUY with a revised target price of INR 4,550 (INR 4,500 earlier) set at 40x Jun’27E EPS

* Strong 1Q performance, PAT +30% YoY growth: 1Q revenue at INR 26bn, +26% YoY was a 6% beat on our estimate and 7% beat on consensus estimates. This was driven by strong growth in both, the domestic and export markets. EBITDA grew 20% YoY to INR 2.6bn, (~5% beat on our/consensus estimates) driven by a strong operating performance and lower-than-expected subcontractor expenses. 1Q EBITDA margins stood at 10%, 40bps lower YoY, and in-line with JM and street expectations. 1Q PAT stood at INR 2bn, +30% YoY; 10% ahead of our estimate and a 13% beat on consensus expectations

* Good overall segmental performance, executing well on strategy: In 1Q, KEI’s cable and wires segment witnessed a robust 32% YoY growth in revenue to INR 24.7bn, with EBIT margins in this segment declining 20bps to 10.8%. Further analysing the product-wise revenue split we note that (1) KEI’s EHV business registered a 56% YoY growth in revenue (inherently higher margin business but no major impact given only 5% of total revenue), (2) revenue from high voltage and low voltage cables registered a growth of 50% and 23% YoY respectively, (3) revenue from house wires grew 30% YoY, and (4) EPC business revenue declined 53% YoY to INR 60mn and contributed ~2% to overall business vs 6% last year, in line with the management’s strategy.

* Reiterates revenue and margin guidance: Management reiterated its FY26 revenue guidance of 18% YoY (we believe, can beat). Further, with new capacities coming on board from Sep'25, it indicated a 20% revenue CAGR over 2-3 years. For FY26 management indicated an 11% EBITDA margin (includes forex gains), and further improvement thereon, which should be driven by a rise in exports, growing orders in EHV cables, and savings in freight costs as the Sanand facility ramps up.

* Sanand greenfield expansion on track: KEI’s INR 20bn greenfield capacity in Sanand is expected to go live in phases. Phase 1, (LV and HV cables), will commence by Sept’25 and further, the entire project will be completed by 1HFY27. Of the INR 20bn, INR 12bn is being incurred to augment EHV capacities. As far as capex spend on this facility is concerned, KEI has spent a total of INR 8.8bn, of which INR 2.9bn was incurred in 1Q. An incremental INR 6-7bn is expected in FY26 and INR 3-4bn is expected in FY27.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361