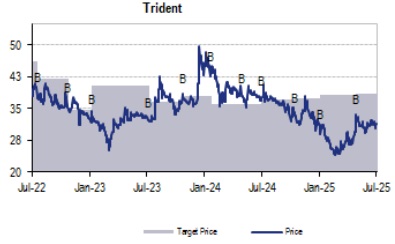

Buy Trident Ltd For Target Rs. 38 By JM Financial Services

Trident reported consol. 1Q EBITDA of INR2.9bn, significantly higher than JMfe of INR2.3bn. Revenue from home–textile segment witnessed de-growth of 4% YoY while revenue from paper segment increased by ~5% YoY. Textile segment EBIT margins came in at 8.8% during the quarter vs. 7.4% last year while margins for the paper segment declined sharply YoY to 28.2% vs. 32.4% in CQLY. Consolidated EBITDA margin expanded by 410bps (17.1% vs. 12.9% in CQLY) driven by lower costs vis-à-vis sales. Net debt decreased to INR8.8bn as at end of 1QFY26 vs INR9.1bn as at end of 4QFY25, a reduction of INR0.3bn. Key margin initiatives taken by the company include a) developing differentiated products leveraging consumer behavior to earn premium b) catering to luxury, fashion accents and sports segments c) increasing CU of plants through digitization and adopting lean practices. We believe a relatively stable cotton price outlook and the Government of India’s continued focus on strengthening the textile ecosystem are likely to support earnings. Trident’s focus on innovative product pipelines, combined with possible positive tailwinds from recent US tariff revisions and India - UK FTA positions the company to capitalize on emerging opportunities. Maintain BUY.

* Consol. margins expand YoY / QoQ: Consol. revenue stood at INR17bn, down ~2% YoY driven by subdued performance in the home textile (down 4% YoY) and paper & chemicals segments (+5% YoY). EBITDA margins came in at 17%, an increase of 410bps YoY driven by lower costs vis-à-vis sales. Consol. PAT increased ~90% YoY to INR1.4bn from INR0.74bn in CQLY. Net debt currently stands at INR8.8bn in Q1FY26 vs. INR9.1bn in Q4FY25, a reduction of INR0.3bn QoQ.

* Segmental performance strong led by paper segment: The quarterly revenue for the home textile segment came at INR18.4bn vs. INR19.7bn in 4Q, an increase of ~6.5% sequentially. EBIT Margin for the segment came in at 8.8%, up 140bps YOY (7.4% in CQLY). The quarterly revenue in Paper & Chemicals segment came in at INR2.6bn vs. INR2.5bn CQLY, an increase of 5% YoY. The EBIT margin for the segment declined YoY by 400bps to 28.2% in 1Q.

* Strategic margin initiatives outlined: Key margin initiatives taken by the company include a) developing differentiated products leveraging consumer behaviour to earn premium b) catering to luxury, fashion accents and sports segments c) increasing CU of plants through digitization and adopting lean practices. We believe a relatively stable cotton price outlook and the Government of India’s continued focus on strengthening the textile ecosystem are likely to support earnings. Trident’s focus on innovative product pipelines, combined with possible positive tailwinds from recent US tariff revisions and India - UK FTA positions the company to capitalize on emerging opportunities.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361