Buy Tega Industries Ltd For Target Rs. 2,025 By JM Financial Services

New Product launches to drive incremental growth

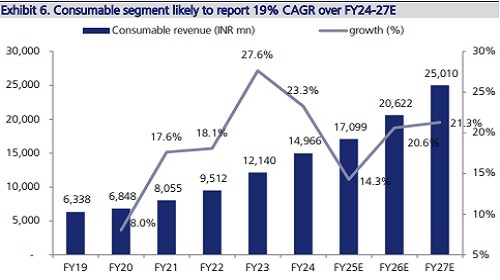

Tega Industries (Tega) is the 5th largest manufacturer of mill liner globally and the second largest manufacturer of polymer-based mill liner. Sector dynamics place Tega in a sweet spot due to a) long lead/conversion time, creating entry barriers, b) no dependency on mining capex (caters to consumable products), c) depleting ore grade and d) continued demand for metals such as copper and gold (75-80% of Tega’s revenue is derived from these two metals). Sales of DynaPrime, launched as a replacement to metallic mill liner (USD 900mn1,000mn market), is progressing as per the management's expectations. DynaPrime margins are currently at par with those of traditional mill liner as it is currently in the initial phase; however, with increasing adoption, it is likely to command better margins, thereby driving overall margins for the consumable segment. The acquisition of McNally Sayaji Engineering Ltd (MSEL) also paved the way for Tega to enter the global mining equipment market. Focus on operational efficiency, integration synergies kicking in, focus on cost reduction, and the increasing service business will likely drive margin expansion for the equipment business. Overall we expect revenue and earnings CAGR of 18.8%/25.6% over FY24-27E, factoring in c.16% revenue CAGR in the equipment business.

* Continued focus on new product development: Tega has been continuously working on new product development as well as smart & green products across product categories to capitalise on opportunities in mining and mineral processing industries. One off-the-key launch of Tega was “DynaPrime” in 2018, which opened up an additional TAM of USD 900mn (focus on converting metal mill liner) in addition to its existing USD 400mn rubber and PM liner market, driving additional revenue for the company; it is also likely to be the key growth driver for the consumable business, going forward. DynaPrime margins are still at par with traditional mill liner margins, but as demand for the product grows with increasing adoption, it is expected to command a premium.

* Equipment margins to improve driven by focus on cost reduction and synergies kicking in: Tega McNally Minerals Ltd. (erstwhile MSEL) reported EBITDA margin of 8.7% in FY24 vs. negative EBITDA margin of 13.4% in FY23 (Tega acquired MSEL in 4QFY23), mainly due to the management's focus on operation efficiency, integration synergies kicking in, and focus on cost reduction. The company is also focussing aggressively on the service business and increase its contribution in the equipment business. Going forward, we expect revenue CAGR of 16% over FY24-27E, with EBITDA margin of 10%-12.5% driven by implementation of cost-efficiency measures and increasing service revenue.

* Maintain BUY with TP of INR 2,025: We remain positive on the stock factoring in a) healthy penetration opportunity for DynaPrime lines, b) cross-selling opportunity for equipment, c) upcoming Chile plant to tap the LATAM markets and d) expansion in newer geographies. We expect revenue and earnings CAGR of 18.8%/25.6% over FY24- 27E, factoring in 19% revenue CAGR in the consumable business and 16% revenue CAGR in the equipment business. We maintain BUY rating on stock with a TP of INR 2,025 based on 35x FY27E vs. its average PE of c.30x since its listing (Dec’21), factoring in increasing TAM for DynaPrime products, industry dynamics and depleting ore quality driving demand for mining consumables such as mill liner.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361