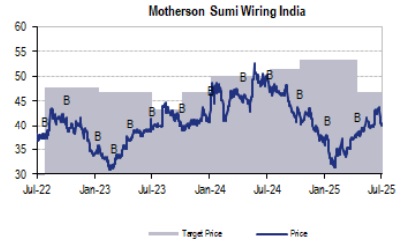

Buy Motherson Sumi Wiring India Ltd For Target Rs. 46 By JM Financial Services

In 1QFY26, Motherson Sumi Wiring India (MSUMI) outperformed the underlying industry with a revenue growth of 14% YoY, 4% below JMFe. EBITDA margin stood at 9.8%, - 110bps below JMFe, led by higher-than-expected increase in employee costs associated with the ramp up of new greenfields and adverse product mix. Excluding the greenfield costs, EBITDA margin stood at 11.8% (vs. 11.7% YoY). Rising features led premiumisation and gradual shift towards EVs (incl. Hybrids) remain the key levers for higher content per vehicle. While the new capacity addition is expected to support medium-term growth, the on-going slowdown in the domestic PV segment and delay in SOPs are likely to weigh on near-term revenue growth. Margins are expected to remain under pressure until the new greenfield facilities achieve full ramp-up. We have reduced our EPS estimates by 4.9% / 3.6% for FY26E / FY27E from our previous estimates. We ascribe 35x PE to arrive at Mar’27 fair value of INR 46. Maintain BUY.

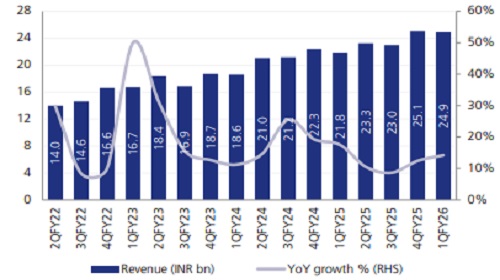

* 1QFY26 – Reported margin below estimates: MSUMI reported revenue of INR 24.9bn (+14% YoY, flat QoQ), 4% below JMFe. Reported EBITDA margin stood at 9.8% (- 110bps YoY, -100bps QoQ), 110bps below JMFe. YoY decline in margins was primarily due to higher employee costs related to the new greenfields and adverse product mix. EBITDA margin (ex-Greenfields) stood at 11.8%. Reported EBITDA came-in at INR 2.4bn (+2% YoY, -10% QoQ), 13% below JMFe. PAT stood at INR 1.4bn (-4% YoY, -13% QoQ), 18% below JMFe.

* Demand Outlook: In 1QFY26, MSUMI’s revenue grew by c.14% YoY, outperforming the underlying industry (+3% YoY), led by higher content per vehicle and new model launches. Revenue contribution from EV stood at 5.4% during the quarter. The management indicated that content per vehicle in EVs is 1.5-1.7x as compared to ICE vehicles. The company commenced operations at its Gujrat greenfield facility (EV) during 1QFY26, with volume ramp-up expected from 2Q onwards. Two additional greenfields (ICE and EV) are expected to be commissioned in FY26. While the ICE greenfield facility in Haryana is on track, the Gujrat facility (EV + ICE) is witnessing delay (due to deferment from OEMs) in SOP from 2QFY26 to 4QFY26. MSUMI has previously indicated that collectively these three greenfields have a peak annual revenue potential of INR 21bn.

* Margin outlook: Gross margin improved 100bps QoQ to 35.3%. Copper prices have inched up during the quarter. However, MSUMI has pass-through arrangement with OEMs for change in copper prices, with a quarter lag. EBITDA margin contracted 110bps YoY to 9.8%, primarily due to higher employee costs associated with the new greenfield facilities. Management indicated that manpower costs will increase gradually with the ramp up of greenfield facilities.

* Other highlights: 1) Capex guidance for FY26 stands at INR 2bn. 2) Net cash stood at INR 160mn as on 1QFY26 end (excluding lease liabilities of ~INR 2.4bn). We transfer coverage to Nitin Agrawal.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361