Buy Balrampur Chini Mills Ltd for the Target Rs. 675 by JM Financial Services Ltd

Balrampur Chini’s 1QFY26 EBITDA was below our estimates due to gross margin contraction. Sugar prices were seen trending downwards sequentially in 1QFY26. Going ahead, we expect sugar volumes to increase gradually while ethanol volumes are likely to pick up pace. The company has initiated PLA imports, which are being used for product development by compounders and converters. The PLA project is on track to be commissioned by 3QFY27. The company aims to achieve optimal utilisation in 6 months. Hence, the PLA business is likely to provide healthy contribution from FY27. We see strong off-take visibility due to support from the UP government for bio-plastics and possible replacement of disposable tableware in India as we have highlighted in our Deep Dive report (click here). If the company is able to achieve its target of full utilisation within 6 months, phase 2 of PLA is definitely on the cards, in our view. In such a case, the company’s shift to specialised products from commodities could be even faster than anticipated. Hence, we retain our constructive stance on the name and maintain BUY with a revised SoTP-based Mar’26 TP of INR 675 (from INR 700 earlier).

* 1QFY26 EBITDA below our expectation: Balrampur’s 1QFY26 gross profit came in 23% below JMFe at ~INR 3.2bn (down 10% YoY) as gross margin was lower than expected at 20.7% (vs. JMFe of 27.5%, ~25% in 1QFY25) while sales was 3% above JMFe at ~INR 15.4bn (up 8% YoY). Other expenses were lower at ~INR 915mn (vs. JMFe of ~INR 1.1bn, ~INR 979mn in 1QFY25). Hence, EBITDA was 35% below JMFe at ~INR 1.3bn (down 19% YoYQ). EBITDA margin was lower at 8.7% (vs. JMFe of 13.8%, ~11.7% in 1QFY25). PAT stood at INR 431mn (down 33% YoY), which was 55% below JMFe.

* Sugar/distillery sales 13%/2% below/above our estimates: Sugar sales was 13% below JMFe at ~INR 11.7bn (up 3% YoY). Sugar volume stood at 254.5KT (vs. JMFe of ~250.4KT, up 4% YoY). Realisation stood at INR 40.6kg (vs. JMFe of INR 40.8/kg and INR 38.8/kg in 1QFY25). Sugar EBIT margin was lower at 4.1% (vs. JMFe: 10% and 6.6% in 1QFY25). As a result, sugar EBIT stood at ~INR 481mn in 1QFY26 (vs. ~INR 747mn in 1QFY25). Distillery sales was 2% above JMFe at ~INR 4.6bn (up 9% YoY). Distillery volume stood at 71.4KL (vs. JMFe of 75KL, up 4% YoY). Realisation stood at INR 58.6/litre (vs. JMFe of INR 60.2/litre and INR 57 in 1QFY25). EBIT margin was higher than expected at 16.8% (vs. JMFe of 15% and 19.1% in 1QFY25). As a result, distillery EBIT stood at ~INR 777mn in 1QFY26 (vs. JMFe of 677mn and INR 811mn in 1QFY25).

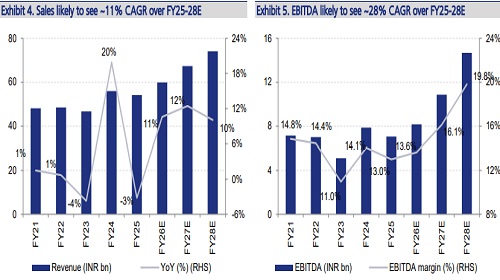

* Estimates lowered by ~4%; maintain BUY: The management has reiterated that the PLA project remains on track to be commissioned by 3QFY27 with optimal utilisation likely to be reached in 6 months. We build in slightly lower sugar prices, considering that prices have been trending downwards in 1QFY26. Based on 1QFY26 results and management commentary, we have revised downwards our FY26-28 EBITDA and EPS estimates by ~4%. We now expect 11%/28%/41% sales/EBITDA/EPS CAGR over FY25-28E. We maintain BUY with a revised SoTP-based Sep'26 TP of INR 675/share (from INR 700 earlier).

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361