Add Titan Company Ltd for the Target Rs.5,000 by Emkay Global Financial Services Ltd

We reiterate ADD on TTAN with Dec-26E TP of Rs5,000 (60x P/E), as our channel checks suggest acceleration in growth momentum in Q4TD (vs ~40% growth in Q3). The growth impetus is backed by TTAN’s studded activation (Festival of Diamonds), merchandise correction, gold exchange/celebrity promotions, and uplift in buyer sentiment in H2 (vs H1). With exponential spike in gold price and weak consumer sentiment, TTAN is currently facing challenges in the under-Rs0.1mn price segment, while other price segments and studded continue to see better buyer growth. In our view, TTAN is improving its merchandise with lightweight and lower-karat jewelry, to address entry-level price points; this should help it deliver a healthy (high-teen) EBIT growth in FY27E. Despite best-in-class EBIT growth of ~25% in 9MFY26, TTAN currently trades ~10% lower than its historical mean and at a discount to other large discretionary players (like DMART). With continued execution, we believe TTAN provides scope for both upward revision to estimates as well as a stock rerating. Key risk: Prolonged disruption in the global gold supply chain

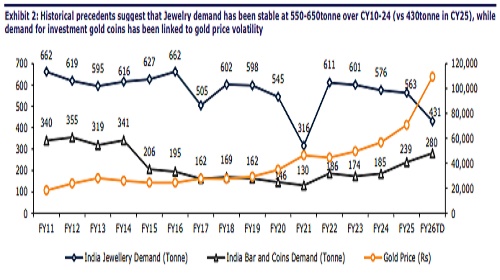

Gold volatility typically impacts only investment demand for the industry

With an exponential spike in gold price, CY25 has seen a dip in jewelry demand in volume terms (down ~24%), while volume for investment-focused gold coins is up ~17% in CY25, per the World Gold Council (WGC). However, historical precedents suggest that Jewelry demand has been stable at 550-650tonne over CY10-24 (vs 430tonne in CY25), while demand for investment gold coins has been linked to gold price volatility (Exhibit 2). In our view, TTAN should be able to deliver a high-teen EBIT growth in FY27E, irrespective of the direction of gold-price movement (Exhibit 1). In the event of continued rise in gold price in FY27, the elevated topline growth should continue, albeit with some margin pain on account of weaker revenue mix and competitive pressure. On the other hand, a stable gold price or a minor gold-price correction in FY27 would bring in fence sitters for jewelry purchase, along with likely muted demand for investment-focused gold coins. We believe that while lackluster demand for gold coins may result in topline growth slowing a bit, the improved revenue mix should result in a similar EBIT growth for TTAN. Over the long term, impact of gold price volatility typically evens out (Exhibit 2); TTAN has consistently clocked a strong 20%+ CAGR in the Jewelry segment in FY16-25.

Pursuing store expansions/new formats to increase TAM

With focus on expanding TAM and warding off the rising competition, TTAN is pursuing a sizable renovation/expansion of its network. The rationale behind the exercise is to capture incremental consumption occasions with dedicated spaces for categories (like wedding and high-value studded/Zoya) and restrict the impact of store openings of new competition in its catchments. TTAN is also experimenting with a standalone store format, Rivaah by Tanishq, for high-ticket wedding purchases – a successful pilot is likely to open an opportunity to expand in top cities; ‘Wedding’ share is currently ~20% for Tanishq.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

.jpg)