Reduce Azad Engineering Ltd for the Target Rs. 1,900 by Choice Institutional Equities

Scaling up Complexity beyond Capacity Expansion

We believe AZAD’s positioning is gradually evolving, and importantly, in the right direction. From what we see, the company is not just adding capacity, but moving towards more complex, mission-critical components. The focus on areas like hot-section parts - where global competition is limited - indicates a clear move up the value chain.

In our view, this is where the real differentiation lies. These are not easy capabilities to build, and once established, they tend to drive better margins and stronger client stickiness. While disclosures remain limited at this stage, the direction of travel is clearly towards higher-value participation.

That said, the next phase is likely to be more about execution than expansion. With multiple plants already set up or ramping up, and inventory built ahead of demand, the key question now is conversion. From FY27 onwards, we expect a shift from investment phase to revenue and cash flow generation.

The ~INR 65,000 Mn order book provides visibility, but in our view, the real inflection depends on efficient transition to a utilisation-led growth cycle. Interestingly, despite a strong backlog, management continues to guide for a measured ~25% growth, which we read as calibrated scaling rather than aggressive ramp-up.

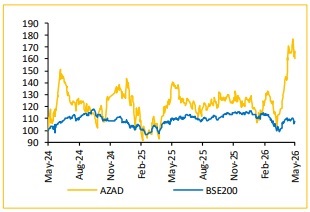

From a valuation perspective, we are factoring in this moderated near-term growth trajectory. Post the recent sharp rally, we downgrade the stock to REDUCE (from BUY), while maintaining our TP of INR 1,900 (45x FY28E EPS).

Miss on Topline, Margin Performance Broadly in line

* Revenue for Q4FY26 grew 27.3% YoY and 1.8% QoQ to INR 1,615 Mn (vs CIE est. INR 1,714 Mn)

* EBITDA for Q4FY26 rose 34.5% YoY but declined 1.4% QoQ to INR 613 Mn (vs CIE est. INR 654 Mn). EBITDA margin stood at 38.0%, up 204 bps YoY and down 124 bps QoQ (vs CIE est. 38.2%)

* PAT for Q4FY26 increased 48.4% YoY and 6.0% QoQ to INR 368 Mn (vs CIE est. INR 386 Mn). PAT margin expanded 324 bps YoY and 91 bps QoQ to 22.8% (vs CIE est. 22.5%)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131