Buy Mrs Bectors Food Ltd for the Target Rs.270 by Motilal Oswal Financial Services Ltd

English Oven & exports to drive growth

We interacted with the management of Mrs Bectors Food (MBFSL) to gain insights into evolving trends across the company’s business segments and its growth outlook. Below are the key highlights from our discussion:

* Domestic Business & Distribution: The company is focused on expanding in lower north markets (UP, Haryana, MP, Rajasthan), with ~80% of distribution additions expected from this region. The company targets adding 40k outlets by FY27 (from ~340k currently), expanding within a 400km radius of its plants, while growth in Punjab may moderate due to rising competition from national players.

* Export & English Oven Expansion: Exports grew in low single digits in 3Q, but management expects mid-to-high teens growth next year, with a focus on adding new customers. Bread capacity expansion is ongoing, with the bun facility already operational and the new bread plant expected to be operational by June. Distribution expansion is planned across Mumbai, Pune, and other markets in Maharashtra, along with entry into the southern market. On QSR, Frozen products currently contribute ~20% of QSR revenues and are expected to be a high-growth segment.

* Financial Outlook: Management guides for mid-teens growth in FY27, with operating margins around ~13.5% by 1HFY27, prioritizing growth in Exports and the English Oven brand, followed by the Domestic and QSR segments

Domestic Biscuits segment to grow in low teens

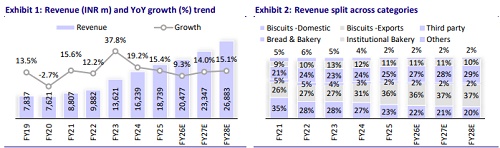

Management highlighted that the bulk of future domestic distribution expansion will be focused on lower north markets, which are expected to account for nearly 80% of total distribution additions. Key markets include UP, Haryana, Madhya Pradesh, and parts of Rajasthan, with UP already emerging as the second-largest market after Punjab, generating revenues of around INR800m. The company expects low-teen growth next year, primarily driven by ~11–12% growth from UP and Haryana, followed by Punjab. However, management indicated that growth from Punjab may moderate as the state is becoming a highly competitive battleground. The distribution strategy involves expanding within a 400km radius around manufacturing plants, with a focus on increasing product distribution per outlet in upper north markets while driving numeric distribution additions in lower north markets. The company currently reaches around 340k outlets and aims to add 40k outlets by FY27. Management stated that major A&P spends will be deployed in Punjab (around 60%), followed by UP and other emerging markets.

Exports continue to grow in mid teens, led by South and Latin America

Exports recorded low single-digit growth in 3Q, primarily due to intensifying competition in Latin America and higher traffic levels in the US market. The current export mix comprises ~7% from the US and 3% from GCC markets of total revenue, with the primary focus on adding new customers. Management expects exports to sustain mid- to high-teens growth over the next two years.

English Oven to be a key growth driver in the domestic business

In the bread segment, capacity expansion is ongoing, with the bun facility already operational, while the new bread factory is expected to commence operations by June. The company is also expanding distribution in Mumbai, Pune, and other parts of Maharashtra within a 300km radius of the Khopoli facility. In southern markets, Hyderabad is currently being serviced through a third-party manufacturing arrangement, while the company has already commenced operations in Bangalore and Kolkata. Additionally, land has been acquired for a new Bangalore plant, which is expected to support demand in southern markets (Chennai & Bangalore) over the next 15 months. Management expects the bread segment to post high-teen growth by FY27.

QSR segment (high single digits) growth led by Frozen Products

Within the QSR segment, frozen products currently contribute around 20% of total QSR revenues, and management expects this category to witness strong growth in the coming years. Overall, the QSR business is projected to deliver high single-digit growth in FY27, with frozen products expected to account for 30% of the segment over the next two years.

Valuation and view: Reiterate BUY

Management expects mid-teens revenue growth over the next two years, while operating margins are likely to remain ~13.5% in 1HFY27. We believe Domestic Biscuits and QSR will remain relatively weaker, with high single-digit growth over the next 2-3 years. Additionally, distribution expansion in the domestic market (especially in the lower north, majorly UP) will remain a key monitorable. We expect BECTORS to deliver a 13% revenue CAGR over FY25-28, driven by: 1) strong growth in domestic bakery, 2) premiumization and health-focused innovation, and 3) growth in export revenues. We reiterate a BUY rating with a DCF-based TP of INR270 (based on an implied P/E of 34x on FY28). Key risks: potential supply chain disruptions impacting production and distribution, and execution risks related to plant consolidation (refer to our IC note dated Jan’26).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041